|

History

>

2008 > USA > Economy (VI)

Oil hits

record

over $143 on Iran-Israel tensions

Mon Jun 30,

2008

1:55pm EDT

Reuters

NEW YORK

(Reuters) - Oil prices hit a record high above $143 a barrel on Monday as

mounting tensions between Iran and Israel stirred supply concerns.

U.S. crude was up 65 cents at $140.86 a barrel by 1:30 p.m. EDT, as weak U.S.

oil demand pulled prices off a record high $143.67 hit earlier. London Brent

crude gained 57 cents to trade at $140.88 a barrel.

The U.S. Energy Information Administration revised downward U.S. April oil

demand by 863,000 barrels per day to 19.77 million bpd -- 3.9 percent below

year-ago levels -- as surging fuel costs erode demand in the world's top

consumer.

The revision showed April demand was the lowest for the month since April 2002,

and came even before prices scaled to new highs in June.

"This revision of the U.S. oil demand for April has certainly put pressure on

crude futures. This is demand destruction before our very eyes," said Phil Flynn

of Alaron Trading. "This is a huge revision, and it happened when (fuel) prices

were still lower, so you can expect that there could be more future downgrades

in demand data."

Crude prices rushed to a fresh high on the weaker dollar and escalating tensions

between Iran, a member of the Organization of Petroleum Exporting Countries, and

Israel over Tehran's nuclear program.

Iran's Revolutionary Guards said Saturday Tehran would impose controls on

shipping in the Persian Gulf and Strait of Hormuz, if it were attacked. Roughly

40 percent of the world's traded oil flows though the narrow waterway separating

Iran from the Arabian Peninsula.

The U.S. Navy's Fifth Fleet said on Monday the United States and its allies

would not allow Iran to hamper shipping in the Gulf. Iran's foreign minister

said Sunday he did not believe Israel was in a position to attack.

Tehran's dispute with the West over its nuclear development program has

supported oil's steep rise this year, as has an influx of cash from investors

seeking to hedge against inflation and the slumping U.S. dollar.

Oil prices have jumped nearly seven-fold since 2002 as part of a broader

commodities rally sparked by surging demand from emerging economies like China

and India.

"Demand from the investment side has been boosted by problems in the financial

sector as well as a desire for diversification," said Frances Hudson, investment

director and strategy and asset manager for Standard Life Investments.

"Also, inflation concerns encourage investment in real assets, such as oil and

gold."

Inflation in the euro zone rose to a record high of 4 percent in June, data

showed Monday.

Oil prices have risen more than 40 percent this year, extending a six-year

rally, in response to the Middle East tensions, plus expectations that supply

will struggle to keep pace with rising demand from emerging economies such as

China and India.

Saudi Oil Minister Ali al-Naimi reiterated his country's position that oil

prices were being driven mostly by speculation and said the OPEC kingpin was

prepared to supply all the oil its customers needed.

The heads of some of the biggest oil companies, gathered at an oil conference in

Madrid, said fundamentals, not investor flows, were the main driver of prices.

"This is a fundamental signal. This is not about speculation," said Tony

Hayward, chief executive of BP Plc.

(Reporting by Matthew Robinson, Gene Ramos, Robert Gibbons in New York; Jane

Merriman in London; Fayen Wong in Perth; Editing by Walter Bagley)

Oil hits record over $143 on Iran-Israel tensions, R,

30.6.2008,

http://www.reuters.com/article/newsOne/idUST14048520080630

Crude

Oil Continues Its Climb

June 28,

2008

The New York Times

By THE ASSOCIATED PRESS

Oil futures

climbed briefly to a new record above $142 a barrel Friday on expectations that

the weakening dollar, a major factor in crude’s stratospheric rise, will extend

its decline and add to oil’s appeal.

Retail gas prices inched lower overnight, but are likely to resume their own

trek into record territory now that oil futures have broken out of the trading

range where they had been for nearly 3 weeks.

Light, sweet crude for August delivery rose as high as $142.26 a barrel in

premarket electronic trading on the New York Mercantile Exchange before pulling

back to trade up $1.05 at $140.69 in late morning trading. On Thursday, the

contract shot past $140 and rose more than $5 to a new settlement record.

Oil rose Thursday in part on comments by OPEC officials; the organization’s

president predicted prices will rise further, and a top Libyan oil official

suggested his nation may cut production.

Meanwhile, traders were coming around to the belief that the dollar, whose long

decline has contributed greatly to oil’s dramatic advance this year, will

continue to weaken.

The stock market’s recent swoon is also sending investors in search of

higher-yielding investments. On Thursday, the Dow Jones industrial average fell

nearly 360 points to its lowest level since September 2006 on a combination of

worries about oil prices and the financial, automotive and technology sectors.

“The renewed attraction of commodities as an investment vehicle is contrasting

with the unattractiveness of the stock market,” said Jim Ritterbusch, president

of energy consultancy Ritterbusch and Associates in Galena, Ill., in a research

note.

“When money has nowhere to go, it is parked in commodities as it is one of the

few investment instruments that actually rises the more money you pour into it,”

said Oliver Jakob, an analyst at Petromatrix Gmbh, in Switzerland in a note.

In other New York trading Friday, July gasoline futures rose 1.64 cents to

$3.5277 a gallon, and July heating oil futures rose 3.53 cents to $3.9187 a

gallon. August natural gas futures rose 10.2 cents to $13.35 per 1,000 cubic

feet.

Michael Grynbaum in New York contributed reporting.

Crude Oil Continues Its Climb, NYT, 28.6.2008,

http://www.nytimes.com/2008/06/28/business/28oil.html

Letters

Our

Corner of the American Dream

June 27,

2008

The New York Times

To the

Editor:

Re “Home Not-So-Sweet Home” (column, June

23):

A renting retiree who used to be a homeowner, I can appreciate Paul Krugman’s

point that home ownership is not for everyone. Indeed, rock music is not for

everyone (I prefer Mozart), nor is eating meat, using public transportation or

having a pet. Everyone’s situation is unique, requiring thoughtful decisions

based on what we believe is best for us and our families.

I would have said it a bit differently: it is not so much home ownership that we

need to look at, but rather the crowd mentality that seems to have afflicted us.

When a particular way of being is deemed “better” by the media, too many of us

get sucked into going along rather than expending the effort necessary to think

things through.

David Zinkin

Princeton, N.J., June 23, 2008

•

To the Editor:

As a 59-year-old woman who has owned a home for the last seven years but rented

in the San Francisco Bay area for two decades before that, I read Paul Krugman’s

column with interest.

Yes, yes, yes, I completely agree that the stigma should be removed from

renting. But for renting to be just as good as ownership in other ways, real

conditions in which renters are forced to live would have to improve as well.

Neighborhoods would have to be safer, and some sort of controls that would

protect tenants from arbitrary rent increases and forced evictions for the

landlord’s convenience and/or profit would have to be in effect.

As an owner, I now know what my monthly mortgage payment will be for the next 25

years, and I know that as long as I make that payment, nobody will decide for me

when I have to move.

Patti Wiley

Davis, Calif., June 23, 2008

•

To the Editor:

Homeownership is the safety net for the middle class. We no longer have job

security. Increasingly, we worry about keeping our health insurance and sending

our children to college.

Until we as a country can find better ways to assist dislocated workers, ensure

access to health care and send our children to college without impoverishing

ourselves in the process, people will continue to aspire to own their own homes,

even though — as Paul Krugman points out — it may not always make sense to do

so.

Karen FitzGerald

Silver Spring, Md., June 24, 2008

•

To the Editor:

Paul Krugman vastly overstates the financial risk of becoming a homeowner.

The peak of the housing bubble from 2005 through early 2007 was a wildly

atypical period for home buyers, many of whom jumped into the market because of

rapidly rising home values, low interest rates and lax mortgage underwriting.

Whether those buyers end up losing their entire financial stake in those homes

that many, especially in the hottest markets, were able to buy with little or no

money down depends upon when they sell them.

Today’s downturn will eventually come to an end, and prices will once again

begin to rise.

It’s always a mistake to compare housing with the stock market. First and

foremost, the vast majority of Americans buy a home as a place to live even

though they can also expect their home equity to grow into their most important

financial asset. As a confessed homeowner himself, Mr. Krugman must know the

difference.

Mr. Krugman is right to suggest that renting opens up a healthy range of housing

options, and he is to be commended for advocating on behalf of the nation’s

renters. But even in a difficult housing downturn, Americans do aspire to become

homeowners, and now more than ever, they deserve the continuation of policies

that enable them to realize that goal.

Jerry Howard

Chief Executive, National

Association of Home Builders

Washington, June 25, 2008

•

To the Editor:

How does one “own” a home, or a car, for that matter, if he is still paying for

it, and it will be taken away if he stops?

Paul Hartman III

Sacramento, June 23, 2008

•

To the Editor:

Paul Krugman’s observations about our uncritical bias in favor of home ownership

and the resulting widespread attitude toward home renters as second-class

citizens calls to mind an exchange I had several years ago while ordering a

pizza.

When I told the delivery dispatcher my address, she asked, “Is that an apartment

or a home?”

I still don’t know what the right answer would have been, though the pizza did

arrive.

James Bloom

Bethlehem, Pa., June 23, 2008

Our Corner of the American Dream, NYT, 27.6.2008,

http://www.nytimes.com/2008/06/27/opinion/l27krugman.html

Worries

About Banks Send Markets Falling

June 27,

2008

The New York Times

By MICHAEL M. GRYNBAUM

Stocks on

Wall Street took a sharp plunge on Thursday after a discouraging report on the

prospects of the nation’s biggest brokerage firms. The Dow Jones industrial

average fell more than 300 points to its lowest level of the year.

A report from Goldman Sachs predicted a new round of write-downs at Citigroup

and Merrill Lynch, and downgraded Citi to a strong “sell” rating.

Shares of Citi slipped 4.8 percent; Merrill Lynch shares were down 5.8 percent.

The sell-off in brokerage firms helped push the Dow down 2.2 percent, past its

intraday low for the year. The blue-chip index is now lower than it was at the

height of the Bear Stearns debacle.

A downgrade of General Motors also put pressure on stocks. Shares of G.M. were

off by 10 percent in midday trading. Shares of Ford were down 3.8 percent

The broader Standard & Poor’s 500-stock index slipped 2.2 percent, or 29 points,

and the technology-heavy Nasdaq composite index was off 2.6 percent.

Many investors had hoped that the investment banks had suffered the worst of the

credit squeeze. But Goldman’s report, released Thursday morning, downgraded the

entire brokerage sector to “neutral,” a sign of decreasing confidence that set

of investors’ already-frayed nerves.

Some had hoped that shares of financial services firms would begin to recover

after nearly a year of painful sell-offs.

Instead, shares fell again, with Bank of America, JPMorgan Chase and Lehman

Brothers all trading lower.

It also became more expensive to guard against the risk of default on bonds from

investment banks. Spreads on credit default swaps widened for most of the major

brokerage firms, an indication decreased confidence in the financial stability

of Wall Street’s marquee names.

Goldman itself suffered a downgrade at the hands of Wachovia, which said the

bank faced a poor outlook over the summer.

Shares of G.M. declined after an analyst at Goldman Sachs cut the company’s

rating, and wrote that the car market could get even worse.Also adding pressure

to the markets was the price of crude oil. In New York, oil was trading up about

$5.20, to $139.75 a barrel. The euro gained against the dollar. Yields fell on

the major Treasury notes, a sign that investors are moving to the relative

safety of government bonds.

Worries About Banks Send Markets Falling, NYT, 27.6.2008,

http://www.nytimes.com/2008/06/27/business/27stox.html?hp

Oil

Prices Jump on OPEC Statements

June 26,

2008

Filed at 2:36 p.m. ET

By THE ASSOCIATED PRESS

The New York Times

NEW YORK

(AP) -- Oil futures shot above $140 Thursday after OPEC's president said oil

prices could rise well above $150 a barrel this year and Libya said it may cut

oil production.

Light, sweet crude for August delivery rose as high as $140.05 in afternoon

trading on the New York Mercantile Exchange before retreating slightly to trade

up $5 at $139.55.

Chakib Khelil, president of the Organization of the Petroleum Exporting

Countries, said he believes oil prices could rise to between $150 and $170 a

barrel this summer before declining later in the year. Khelil said he doesn't

think prices will reach $200 a barrel.

Khelil joins a long list of forecasters who have made bold oil price predictions

this year. Each new forecast -- such as Goldman Sachs' recent prediction that

prices could rise as high as $200 -- causes a jump in prices as speculative

buyers are drawn into the market.

Meanwhile, the head of Libya's national oil company said the country may cut

crude production because the oil market is well supplied, according to news

reports.

''Shokri Ghanem, the nation's top oil official, declined to say when a decision

would be made on whether to lower production, or give any indication of the size

of the cut under consideration,'' said Addison Armstrong, director of market

research at Tradition Energy in Stamford, Conn., in a research note.

Oil's move above $140 a barrel was the first for what's known as a front-month

crude contract, or the contract with the earliest expiration date. But it was

not the August contract's first foray above $140 -- August crude futures rose as

high as $140.42 a barrel while July futures were still traded as the front-month

crude contract. Many other later contracts have also traded above $140.

The previous trading record for a front-month contract was $139.89, set by the

July contract on June 16.

Oil Prices Jump on OPEC Statements, NYT, 26.6.2008,

http://www.nytimes.com/aponline/business/AP-Oil-Prices.html

Fed

Keeps Rates Steady, but Notes Inflation Worries

June 26,

2008

The New York Times

By LOUIS UCHITELLE

Caught

between inflationary pressures and a weakening economy, the Federal Reserve’s

policy makers voted on Wednesday to deal primarily with the weakening economy by

keeping interest rates at their present level.

The decision to hold at 2 percent the key short-term federal funds rate — which

affects what consumers pay for mortgages, car loans and other credit — brought

to a halt a stream of rate cuts since August, reductions that brought the fed

funds rate to its lowest level since November, 2004.

The halt signaled concern among policy makers that they might have to reverse

course by the end of the year if rising oil prices push up the prices of goods

and services across the economy. So far, apart from significant increases in

food and energy, that has not happened.

Still, the Fed, in its statement after the meeting, expressed greater concern

about inflation than it had after its last meeting in April.

“Although downside risks to growth remain, they appear to have diminished

somewhat, and the upside risks to inflation and inflation expectations have

increased,” the statement said. “The committee will continue to monitor economic

and financial developments and will act as needed to promote sustainable

economic growth and price stability.

In the statement, the Fed said that it expected inflation to moderate later this

year and next year, but “in light of the continued increases in the prices of

energy and some other commodities and the elevated state of some indicators of

inflation expectations, uncertainty about the inflation outlook remains high.”

Yet, the statement said: “Labor markets have softened further and financial

markets remain under considerable stress. Tight credit conditions, the ongoing

housing contraction and the rise in energy prices are likely to weigh on

economic growth over the next few quarters.”

The decision was widely expected on Wall Street, where the major stock indexes

showed little reaction. An initial spurt just after the announcement quickly

dissipated.

The Fed’s decision came as reports this week showed that home prices and

consumer confidence continued to decline as foreclosures multiply. There have

been signs that the economy might be stabilizing, but the latest data suggested

that the economy was still unwinding. A rising unemployment rate and shrinking

payrolls as employers shed workers have reinforced the impression of an economy

still in need of help.

“I don’t think we are out of the woods yet, and I don’t think the Fed does

either,” said Lyle E. Gramley, a former Fed governor who is now a senior adviser

at the Stanford Washington Research Group.

Trying to revive the economy, the Fed has cut interest rates to its present

level of 2 percent from 5.25 percent in August, doing so at each of its policy

meetings and at emergency sessions between meetings in the early days of the

crisis over the credit markets.

The reductions have helped. The economy has continued to grow, although not by

much. But it has avoided the outright contraction that marks a recession. And

the Fed’s new lending practices, hastily put together last fall, has channeled

loans not only to banks, to encourage them to continue lending, but to

investment houses that otherwise might collapse.

In the midst of this rescue process, surging oil prices have threatened to raise

the inflation rate and the Fed policy makers, starting with the chairman, Ben S.

Bernanke, recognized this problem in recent speeches, suggesting to Wall Street

that the Fed might raise rates. The policy makers, however, “were surprised by

the intensity of the market’s reaction,” as Ian Sherpherdson, chief United

States economist for High Frequency Economics, put it in a newsletter.

And Nigel Gault, chief domestic economist at Global Insight, added: “At this

point most of Wall Street wants low rates because the financial sector is in

trouble and low rates help that sector.”

So the Fed’s policy makers backed off in subsequent comments, signaling that

they would not raise rates in the near term, thus making credit more expensive,

or lower them, an indication that 2 percent is low enough to stimulate spending

on credit even in a weak economy.

“They are trying to balance concerns about growth against inflation risks,” Mr.

Gault said, “and their answer for the moment, from most of the policy makers, is

that the inflation risk is not big enough to warrant raising rates right now.”

The Fed, in holding rates steady, has placed less importance on inflation than

the European Central Bank. Jean Claude-Trichet, the bank’s president, has

indicated that the European bank may raise short-term rates at its meeting in

July. The European economy, which has not been as hard hit by the housing

slowdown and the tight credit market, has been generally stronger than

America’s, which has helped to make fighting inflation a greater priority.

Nevertheless, Mr. Bernanke has often expressed his concern that failure to act

or to signal the Fed’s determination to suppress inflation would raise

“inflationary expectations,” which means that the public comes to expect prices

to keep rising and acts accordingly. This was an issue in the late 1970s, when

companies raised prices and workers demanded and received wage increases.

Another price increase set off another round of rising wages and in resulting

wage-price spiral, inflation got out of hand — until the Fed, led then by Paul

A. Volcker, suppressed it with huge rate increases that pushed the economy into

a steep recession.

This time, many economists say, a wage-price spiral is not possible because

workers lack the bargaining power, particularly the union bargaining power, to

push up wages. Indeed, they have stagnated in recent years.

“There isn’t a wage-price spiral,” Mr. Gault said. “The public might come to

expect a rising inflation rate, but it isn’t likely to have much influence on

wage setting.”

Fed Keeps Rates Steady, but Notes Inflation Worries, NYT,

26.6.2008,

http://www.nytimes.com/2008/06/26/business/26fed.html?hp

White

House: U.S. economy resilient long term

Tue Jun 24,

2008

12:56pm EDT

Reuters

WASHINGTON

(Reuters) - The White House said on Tuesday, after data showing U.S. consumer

confidence fell to a 16-year low, the long-term resiliency of the U.S. economy

was very strong.

"We know that Americans are concerned about the economy, we have been concerned

about the economy," White House spokeswoman Dana Perino said.

But she also said it was going to take a while for the economic stimulus package

to take effect and for that to be reflected in economic data, such as retail

sales.

"We are confident that it will have the impact that we thought it would toward

the latter half of the year. We believe that the long-term resilience of our

economy is very strong," Perino said.

(Reporting by Tabassum Zakaria)

White House: U.S. economy resilient long term, R,

24.6.2008,

http://www.reuters.com/article/newsOne/idUSWBT00926120080624

House

prices, consumer confidence dive

Tue Jun 24,

2008

1:23pm EDT

Reuters

By Lynn Adler

NEW YORK

(Reuters) - Consumer sentiment slid to a 16-year low in June while house prices

suffered record annual drops in April, according to data Tuesday that suggested

a retrenchment in spending that will keep squelching economic growth.

The Conference Board's monthly survey of consumers showed the overall index of

consumers' mood fell to 50.4 in June, the lowest since 47.3 in February 1992.

The index has now dropped by more than half since 111.90 last July, before the

housing market troubles triggered the most severe credit crisis in at least a

decade.

"To put it in perspective, that's a bigger decline than what we saw after the

September 11 attack and Hurricane Katrina," said Dana Saporta, economist at

Dresdner Kleinwort Securities.

"It sends out the signal that the consumers are not about to ramp up their

spending," she said. "We worry about the contraction in the economy once the tax

rebates dissipate."

In addition, the survey showed an index measuring consumer expectations for the

future sank to a record low as inflation forecasts matched an all-time high this

month.

The inflation threat has been highlighted in the past 24 hours by massive price

increases announced by some of the world's largest basic materials

conglomerates.

First, mining titan Rio Tinto secured an agreement with China's largest steel

maker to nearly double the price Rio gets for iron ore, and rival producer BHP

Billiton is expected to follow through with similar price hikes.

Then early Tuesday, Dow Chemical Co. said it would raise prices up to 25

percent, just weeks after the largest U.S. chemicals maker implemented a 20

percent across-the-board price increase.

U.S. home prices in April, meantime, extended their record annual slump in April

although the pace of decline subsided a bit in the month, according to Standard

& Poor's/Case-Shiller data.

S&P's 20-city index for April posted a smaller-than-expected 1.4 percent drop

from March, but it also slumped by a record 15.3 percent annually and by 17.8

percent since hitting its peak in July 2006.

By another measure, the Office of Federal Housing Enterprise Oversight, which

gauges prices based on relatively low risk loans purchased by Fannie Mae and

Freddie Mac, said its home price index fell 0.8 percent in April from March for

a 4.6 percent annual downturn.

Both housing reports suggest consumers will be less in the mood to ramp up

spending any time soon.

However, U.S. Treasury Secretary Henry Paulson said on Tuesday he thought that

most of the slump in U.S. housing prices would be over by year end and that

growth should be stronger by then.

In an interview on Mexican television, Paulson said the global economy was being

strained by costly energy but said U.S. economic fundamentals were sound.

"I feel moderately optimistic that at the end of the year we will have signs of

an economic recovery," Paulson said. "Hopefully the biggest part of the housing

decline will be over by the end of the year."

(Additional reporting by Richard Leong and Burton Frierson in New York and Glenn

Somerville and Jason Lange in Cancun, Editing by Chizu Nomiyama)

House prices, consumer confidence dive, R, 24.6.2008,

http://www.reuters.com/article/newsOne/idUSN2433847420080624

Op-Ed

Columnist

Home Not-So-Sweet Home

June 23,

2008

The New York Times

By PAUL KRUGMAN

“Owning a

home lies at the heart of the American dream.” So declared President Bush in

2002, introducing his “Homeownership Challenge” — a set of policy initiatives

that were supposed to sharply increase homeownership, especially for minority

groups.

Oops. While homeownership rose as the housing bubble inflated, temporarily

giving Mr. Bush something to boast about, it plunged — especially for

African-Americans — when the bubble popped. Today, the percentage of American

families owning their own homes is no higher than it was six years ago, and it’s

a good bet that by the time Mr. Bush leaves the White House homeownership will

be lower than it was when he moved in.

But here’s a question rarely asked, at least in Washington: Why should

ever-increasing homeownership be a policy goal? How many people should own

homes, anyway?

Listening to politicians, you’d think that every family should own its home — in

fact, that you’re not a real American unless you’re a homeowner. “If you own

something,” Mr. Bush once declared, “you have a vital stake in the future of our

country.” Presumably, then, citizens who live in rented housing, and therefore

lack that “vital stake,” can’t be properly patriotic. Bring back property

qualifications for voting!

Even Democrats seem to share the sense that Americans who don’t own houses are

second-class citizens. Early last year, just as the mortgage meltdown was

beginning, Austan Goolsbee, a University of Chicago economist who is one of

Barack Obama’s top advisers, warned against a crackdown on subprime lending.

“For be it ever so humble,” he wrote, “there really is no place like home, even

if it does come with a balloon payment mortgage.”

And the belief that you’re nothing if you don’t own a home is reflected in U.S.

policy. Because the I.R.S. lets you deduct mortgage interest from your taxable

income but doesn’t let you deduct rent, the federal tax system provides an

enormous subsidy to owner-occupied housing. On top of that, government-sponsored

enterprises — Fannie Mae, Freddie Mac and the Federal Home Loan Banks — provide

cheap financing for home buyers; investors who want to provide rental housing

are on their own.

In effect, U.S. policy is based on the premise that everyone should be a

homeowner. But here’s the thing: There are some real disadvantages to

homeownership.

First of all, there’s the financial risk. Although it’s rarely put this way,

borrowing to buy a home is like buying stocks on margin: if the market value of

the house falls, the buyer can easily lose his or her entire stake.

This isn’t a hypothetical worry. From 2005 through 2007 alone — that is, at the

peak of the housing bubble — more than 22 million Americans bought either new or

existing houses. Now that the bubble has burst, many of those homebuyers have

lost heavily on their investment. At this point there are probably around 10

million households with negative home equity — that is, with mortgages that

exceed the value of their houses.

Owning a home also ties workers down. Even in the best of times, the costs and

hassle of selling one home and buying another — one estimate put the average

cost of a house move at more than $60,000 — tend to make workers reluctant to go

where the jobs are.

And these are not the best of times. Right now, economic distress is

concentrated in the states with the biggest housing busts: Florida and

California have experienced much steeper rises in unemployment than the nation

as a whole. Yet homeowners in these states are constrained from seeking

opportunities elsewhere, because it’s very hard to sell their houses.

Finally, there’s the cost of commuting. Buying a home usually though not always

means buying a single-family house in the suburbs, often a long way out, where

land is cheap. In an age of $4 gas and concerns about climate change, that’s an

increasingly problematic choice.

There are, of course, advantages to homeownership — and yes, my wife and I do

own our home. But homeownership isn’t for everyone. In fact, given the way U.S.

policy favors owning over renting, you can make a good case that America already

has too many homeowners.

O.K., I know how some people will respond: anyone who questions the ideal of

homeownership must want the population “confined to Soviet-style concrete-block

high-rises” (as a Bloomberg columnist recently put it). Um, no. All I’m

suggesting is that we drop the obsession with ownership, and try to level the

playing field that, at the moment, is hugely tilted against renting.

And while we’re at it, let’s try to open our minds to the possibility that those

who choose to rent rather than buy can still share in the American dream — and

still have a stake in the nation’s future.

Home Not-So-Sweet Home, NYT, 23.6.2008,

http://www.nytimes.com/2008/06/23/opinion/23krugman.html?ref=opinion

Gas

prices climb to record $4.10

Mon Jun 23,

2008

1:25pm EDT

Reuters

By Martinne Geller

NEW YORK

(Reuters) - Gasoline is costing U.S. drivers a record $4.10 per gallon on

average, but pump prices may be at a peak and could start to come down, an

industry analyst said on Sunday.

That optimism is linked to a pledge by Saudi Arabia to pump more oil in response

to consumer countries' requests, according to Trilby Lundberg, editor of the

nationwide Lundberg survey of about 7,000 gas stations.

"I suspect that oil prices have peaked and will flip further because of this

news and the physical addition of more oil on the market in July," Lundberg

said. "This gives a strong chance that pump prices are peaking now, or may

already have done so."

A barrel of oil has doubled in price over the past year, stoking inflation,

triggering protests from Asia to Europe, and compounding the financial pain of

U.S. consumers already grappling with a sagging housing market, job uncertainty

and soaring food costs.

Top officials, policy makers and oil company executives met on Sunday in Jeddah,

Saudi Arabia, for emergency talks on how to bring prices down.

"Crude oil prices may spike at any moment from existing trouble in areas

including Nigeria, or from some unforeseen hit to global supply," Lundberg said.

"This may sound optimistic, (but) it seems likely at this moment as the meeting

in Jeddah, Saudi Arabia is being concluded, that oil prices may have peaked and

may drift down."

One common reason cited for the rise of oil prices is soaring demand from

developing economies such as India and China, whose emerging middle classes are

gobbling up more oil.

Lundberg said it was unclear whether other countries with fuel subsidies would

follow China's lead and cut them in efforts to cap demand.

Demand in the United States has fallen about 1 percent year-to-date, though it

is closer to 2 percent lower in recent weeks, Lundberg said.

Prices at the pump vary across the country. The luckiest drivers live in Tulsa,

Oklahoma, where the city average was $3.76 per gallon, the nation's lowest. At

the other end, Los Angeles and Fresno, California, were tied for the nation's

most expensive gasoline, with the city averages reaching $4.59 per gallon of

regular grade gasoline.

On June 20, U.S. crude closed at $134.71 per barrel, up from $68.19 a year ago.

(Editing by Phil Berlowitz)

Gas prices climb to record $4.10, R, 23.6.2008,

http://www.reuters.com/article/domesticNews/idUSN2244992620080623

Ford

Delays Pickup as Big Vehicle Slump Hurts Outlook

June 21,

2008

The New York Times

By NICK BUNKLEY

DEARBORN,

Mich. — The Ford Motor Company said on Friday that it would delay introducing

its new pickup truck and that it will probably lose money for a fourth

consecutive year in 2009 because of the slowdown in demand for large vehicles.

Ford said it would begin selling the highly anticipated 2009 version of the

F-150 pickup in late fall, two months later than intended, so that dealers would

have more time to clear out the current model. In addition to the delay, the

company said it would build 90,000 fewer trucks in the second half of the year

than it had previously planned, while increasing production of cars and

crossovers that are more fuel-efficient.

“As gasoline prices average more than $4 a gallon and consumers worry about the

weak U.S. economy, we see June industry-wide auto sales slowing further and

demand for large trucks and S.U.V.’s at one of the lowest levels in decades,”

Ford’s chief executive, Alan R. Mulally, said in a statement. “Ford has taken

decisive action to respond to this accelerating shift in customer demand away

from large trucks and S.U.V.’s to smaller cars and crossovers, and we will

continue to act swiftly moving forward.”

For the second time in a month, Ford issued a warning about next year’s

financial results. “Unless the economy improves, it will be difficult for Ford

to break even companywide on a pretax basis in 2009, excluding special items,”

the statement said. In May, executives had abandoned Ford’s long-held goal of

becoming profitable in 2009, predicting a break-even performance.

The automaker said the market had deteriorated to such a degree that its

financing arm, Ford Motor Credit, which has been a dependable source of profit,

would lose money this year.

Losses from automotive operations would be worse this year than in 2007, the

statement said, the opposite of its previous guidance. Ford lost $2.7 billion

overall in 2007 and has not earned a full-year profit since 2005.

Ford Credit will have a pre-tax loss — excluding any potential payment related

to Ford’s profit maintenance agreement — primarily because of further weakness

in large truck and S.U.V. auction values. Ford Credit is no longer is planning a

distribution payment to Ford in 2008.

Shares of Ford fell nearly 6 percent, to $5.96, in morning trading.

The F-150 delay increases the likelihood that the F-series will lose its

distinction as the best-selling vehicle in the United States after 31

consecutive years. In May, four Japanese sedans, led by the Honda Civic, outsold

the F-series, the first time in 16 years that a pickup truck was not the top

seller in any given month. Sales of the F-series fell 33 percent last month and

are down 20 percent so far this year.

Ford has spent several years and hundreds of millions of dollars, if not

billions, overhauling the F-150, which has generated huge profits and is

responsible for a large part of Ford’s image. It is one of two new full-size

pickups scheduled to go on sale this fall, along with Chrysler’s 2009 Dodge Ram.

Chrysler executives said they had no plans to delay the Ram’s launch.

“There’s no better way to fight a slower pickup market than to introduce what we

think is a game-changing truck,” a Chrysler spokesman, Bryan Zvibleman, said.

General Motors announced earlier this month that it would close four truck

plants in North America, and more recently has decided to pull back on plans to

revamp its pickups and S.U.V.’s in order to focus attention on smaller cars.

Because of the precipitous drop in demand for trucks, Ford said it now expected

total industry sales to be 14.7 million to 15.2 million vehicles, down from its

previous projection of at least 15 million.

Analysts say the first three weeks of June have been particularly dismal, with

J.D. Power and Associates estimating that sales are equal to an annualized rate

of 12.5 million vehicles, the worst in at least 15 years.

In response, Ford is shutting its truck plant in Wayne, Mich., for nine weeks

starting Monday, though the adjacent car plant, which builds the fast-selling

Focus sedan, is adding a third shift and increasing the speed of its assembly

line.

The company will eliminate a shift at each of the two plants that build the

F-150, in Kansas City and Dearborn. The Dearborn plant will be idle for “most of

the third quarter,” Ford said. Meanwhile, a sport-utility vehicle plant in

Louisville will lose a shift in the third quarter.

In contrast, shifts will be added to a plant in Ontario that builds crossover

vehicles and to the assembly line in Kansas City that builds Ford’s most

fuel-efficient S.U.V.’s, including hybrid versions.

“We view the move to smaller, more fuel-efficient vehicles as permanent, and we

are responding to customer demand,” Mr. Mulally said. “In the near term, we are

adjusting production to the actual demand — increasing small cars and crossovers

and reducing large trucks and S.U.V.’s. For the long term, we are moving fast to

introduce more small cars, crossovers and fuel-efficient powertrains — including

more hybrids.”

Ford Delays Pickup as Big Vehicle Slump Hurts Outlook,

NYT, 21.6.2008,

http://www.nytimes.com/2008/06/21/business/21ford.html?hp

Oil

Nears $140 a Barrel; Weak Dollar Cited

June 17,

2008

The New York Times

By THE ASSOCIATED PRESS

Oil futures

are hitting a new milestone near $140 a barrel, a dramatic surge analysts

attributed to the weakening dollar. The surge comes even despite expectations

that Saudi Arabia, the world’s biggest oil exporter, was planning to increase

its output by about a half-million barrels a day.

Light, sweet crude for July delivery rose to a trading record of $139.89 a

barrel Monday, but retreated slightly to trade up $3.45 at $138.31 a barrel on

the New York Mercantile Exchange.

The dollar fell on a weak report on New York state manufacturing activity,

analysts said. Many investors buy commodities like oil as a hedge against

inflation when the dollar falls. Also, a weaker dollar makes oil less expensive

to investors dealing in other currencies.

Many analysts believe the dollar’s protracted decline is a major factor behind

oil’s doubling in price over the last year.

Plans by Saudi Arabia to increase production could bring its output to a level

of 10 million barrels a day, which, if sustained, would be the kingdom’s highest

ever. The move was seen as a sign that the Saudis are becoming increasingly

nervous about both the political and economic effect of high oil prices.

Saudi Arabia is currently pumping 9.45 million barrels a day, which is an

increase of about 300,000 barrels from last month.

While they are reaping record profits, the Saudis are concerned that today’s

record prices might eventually damp economic growth and lead to lower oil

demand, as is already happening in the United States and other developed

countries. The current prices are also making alternative fuels more viable,

threatening the long-term prospects of the oil-based economy.

Oil Nears $140 a Barrel; Weak Dollar Cited, NYT,

17.6.2008,

http://www.nytimes.com/2008/06/17/business/worldbusiness/17oil.html

Foreclosures Rose Again in May

June 14,

2008

The New York Times

By THE ASSOCIATED PRESS

WASHINGTON

— The number of homeowners swept up in the housing crisis rose last month, with

foreclosure filings up nearly 50 percent compared with a year earlier, a

foreclosure listing company said Friday.

Nationwide, 261,255 homes received at least one foreclosure-related filing in

May, up 48 percent from 176,137 in the same month a year ago and up 7 percent

from April, the listing company, RealtyTrac, said.

One in every 483 households received a foreclosure filing in May, the highest

number since RealtyTrac started the report in 2005 and the second-consecutive

monthly record.

Foreclosure filings increased from a year earlier in all but 10 states, with

Arizona, California, Florida, Michigan and Nevada having the highest statewide

foreclosure rates.

Metropolitan areas in California and Florida accounted for 9 of the top 10 areas

with the highest rate of foreclosure. That list was led by Stockton, Calif. and

the Cape Coral-Fort Myers area in Florida.

RealtyTrac monitors default notices, auction sale notices and bank

repossessions. Nearly 74,000 properties were repossessed by lenders nationwide

in May, while more than 58,000 received default notices, the company said.

In Nevada, one in every 118 households received a foreclosure-related notice

last month, more than four times the national rate. In California, one in every

183 households faced foreclosure.

The combination of weak housing sales, falling home values, tighter mortgage

lending criteria and a slowing economy has left financially strapped homeowners

with few options to avoid foreclosure.

Rick Sharga, RealtyTrac’s vice president for marketing, said foreclosures were

unlikely to peak until sometime this fall, as more loans made to borrowers with

poor credit records reset at higher levels.

About 50 to 60 percent of borrowers who receive foreclosure filings will

probably lose their homes, Mr. Sharga said. The rest are likely to be able to

sell or refinance.

Foreclosures Rose Again in May, NYT, 14.6.2008,

http://www.nytimes.com/2008/06/14/business/14mortgage.html

Oil and

Food Push Consumer Prices Higher in May

June 14,

2008

The New York Times

By MICHAEL M. GRYNBAUM

Inflation

hit hard in May as prices for a wide swath of consumer goods rose at their

fastest pace in six months, underscoring warnings from central bankers and

adding to a growing consensus that the Federal Reserve might raise interest

rates by the end of the year.

The Consumer Price Index, which measures prices of a batch of common household

products, rose 0.6 percent last month, as Americans were forced to cope with a

sharp increase in fuel costs. The report, released Friday by the Labor

Department, is considered a benchmark measure of inflation.

On Wall Street, the major stock indexes rose after the report, with the Standard

& Poor’s 500-stock index up 1.3 percent before 10:30 a.m. The Dow Jones

industrials gained more than 140 points.

The index, which rose more than economists had forecast, comes on the heels of

repeated warnings about inflation from the world’s central banks. Ben S.

Bernanke, the chairman of the Fed, joined other top officials this week in

focusing on higher prices, citing the economic damage wrought by the record

run-up in food and oil prices around the world.

The speeches have fueled a growing sense on Wall Street that the Fed has shifted

its focus from supporting growth to fighting inflation. The May C.P.I. will

probably heighten expectations that higher interest rates, which tend to hold

down prices, may be in the offing.

In May, gasoline prices rose 5.2 percent, and were up 21 percent compared with a

year ago, according to the report. They may rise again in June: the nationwide

average for gasoline topped $4 a gallon last weekend as the price of oil leaped

to a new high.

The cost of eating rose, as well, as Americans paid 5 percent more for foods and

beverages in May than a year ago.

On an annual basis, inflation worsened for the first time in three months,

reversing a downward trend. Inflation ran at 4.2 percent in May compared with a

year ago.

High oil prices also pushed up costs for other products, as businesses, squeezed

by higher shipping and production costs, sought to raise the prices paid by

their customers. Prices for transportation, commodities, tobacco and utility

fuels all increased for the month. Excluding the cost of food and gasoline,

inflation ran at 0.2 percent for the month.

“Both consumers and financial market participants are becoming sensitized to

large headline price rises, and were especially ready this month amid heightened

inflation anxiety,” Peter Kretzmer, an economist at Bank of America, wrote in a

note.

Consumers, however, do not appear content with rising prices. A measure of

Americans’ confidence in the economy fell to its lowest level since 1980,

another period of high inflation and slow growth. The University of Michigan’s

consumer confidence survey dropped to 56.7 in June, the fifth consecutive month

of decline.

Oil and Food Push Consumer Prices Higher in May, NYT, 14.6.2008,

http://www.nytimes.com/2008/06/14/business/14econ.html?hp

Stocks

Rise on Retail Sales Figures

June 13,

2008

The New York Times

By MICHAEL M. GRYNBAUM

Wall Street

warmed to strong sales numbers on Thursday, as stocks moved higher on a sign of

some resilience in the primary engine of the economy.

The Dow Jones industrials gained 170 points, erasing its losses for the week,

after the Commerce Department reported that retail sales rose more than expected

last month.

“The sharp improvement in May was clearly driven by receipt of the first wave of

tax rebate payments,” Joshua Shapiro, chief United States economist at the

research firm MFR, wrote in a note. “These payments will continue to be a

positive factor for the consumer in the next couple of months.”

Some economists remained skeptical that May’s sales bump would continue.

“Once one begins to look over the horizon for a catalyst to support consumption,

all that remains is a stressed consumer whose purchasing power is rapidly being

reduced by the ravages of inflation,” Joseph Brusuelas, an economist at Merk

Investments, wrote in a note.

But even as Americans headed to the mall, they faced higher prices when they got

there. A separate measure of import prices rose sharply in May, driven up by

expensive oil and the comparatively weak dollar.

That report will play into the fears of inflation that have been aired by

Federal Reserve policy makers over the last few weeks. A rise in import prices

offers further evidence that Americans are being pressured by higher prices,

with little letup expected in the coming months.

Though Wall Street rallied on the developments — the broad Standard & Poor’s

500-stock index was up more than 1 percent before noon — the data could open the

door for the Fed to raise interest rates or keep them steady over the next few

months. The yield on the two-year Treasury bond, a gauge for investors’ interest

rate expectations, was up more than a tenth of a percentage point, a relatively

big one-day rise.

Rate increases tend to curb inflation, but shut off economic growth. The retail

sales report is considered a good gauge for consumer spending, which accounts

for more than two-thirds of the nation’s economic activity. Last month’s pickup

in sales suggested that the economy may be resilient enough to withstand a rise

in rates.

Sales of retail goods and services rose 1 percent last month, twice the expected

increase. Sales were strongest at gasoline stations, a likely result of the

record gain in oil prices during the survey period. But sales at general

merchandise outlets, which can include thrift shops and dime stores, climbed 1.2

percent, evidence that Americans were trying to cut down on more expensive

items.

The government also revised up its estimates for previous months, reporting that

April sales increased 0.4 percent, compared with an initial drop of 0.2 percent,

and March sales went up 0.5 percent, compared with an earlier reading of a 0.2

percent increase.

The better-than-expected report may be tempered by last month’s surge in the

price of imports. In a separate report on Thursday, the Labor Department said

that import prices rose 2.3 percent in May after a 2.4 percent rise in April.

Compared with readings a year earlier, import prices have grown by nearly 18

percent; excluding oil, the rise was 6.6 percent. Energy products fueled much of

the increase, with petroleum imports gaining 7.8 percent last month.

A separate report from the Labor Department showed that the number of workers

who filed first-time claims for unemployment benefits rose 25,000, to 384,000,

in the week ended June 7.

The Commerce Department also said that business inventories rose 0.5 percent in

April, up from 0.2 percent in March. Retailers and wholesalers reported the

biggest gains in inventories, while manufacturers stayed flat.

Stocks Rise on Retail Sales Figures, NYT, 13.6.2008,

http://www.nytimes.com/2008/06/13/business/13econ.html?hp

Lehman

Posts Loss and Plans to Raise Capital

June 10,

2008

The New York Times

By JENNY ANDERSON and LOUISE STORY

Lehman

Brothers, seeking to ally concern that it might become the next Wall Street bank

to founder, said Monday that it would raise $6 billion to shore up its weakened

finances.

The move came as the investment bank stunned Wall Street with news that it had

lost $2.8 billion in the second quarter, its first loss since going public in

1994. The deficit far exceeded even the most pessimistic forecasts and reflected

a triple blow of soured assets, bad trades, and hedges that were supposed to

cushion losses but instead added to them.

The developments mark a stark turnabout for the scrappy Lehman, which had

repeatedly assured shareholders that it was managing its risks well. Many

investors have feared for Lehman’s health since Bear Stearns collapsed, and the

red ink at the bank could fuel the debate over whether Lehman, one of the

smallest players on Wall Street, can survive as an independent firm.

“I am very disappointed in this quarter’s results,” Richard S. Fuld, Lehman’s

chairman and chief executive, said in a statement.

Erin Callan, Lehman’s chief financial officer, said Monday that the bank had

moved aggressively to reduce its leverage and bolster confidence among its

investors. In addition to raising fresh capital by selling common stock and

convertible preferred shares, Lehman has sold about $130 billion in assets since

April, Ms. Callan said on a conference call.

"It’s designed to end the chatter of Lehman Brothers, and let us get back to

business," Ms. Callan said of the new capital. Lehman does not expect to sell

more assets or raise more money, she said.

Such assurances aside, Lehman may not be out of the woods. The firm has been

engaged in a very public battle with short-sellers who have questioned the way

Lehman values many illiquid assets, like residential and commercial mortgages,

and who have questions on the aggressive leverage the firm has engaged in.

Investors were particularly concerned about Lehman’s leverage level considering

its small equity base. In a statement, the firm said it reduced gross leverage

to 25 from 31.7 — borrowing $25 for every $1 of equity — at the end of the first

quarter and reduced net leverage to less than 12.5 from 15.4.

But after seemingly weathering the storm in the credit markets, Lehman now joins

the ranks of banks like Merrill Lynch and Citigroup, which have suffered

billions of dollars of write-downs and have been forced to raise tens of

billions of dollars in capital. Moody’s Investors Service downgraded its outlook

on Lehman to negative from stable on Monday, citing insufficient hedges and

continued exposure to troubled sectors. Fitch Ratings cut Lehman’s credit rating

to A+ from AA-.

Lehman’s shares were off $2.90, or about 9 percent, to $29.39 at 1 p.m. They are

down more than 50 percent this year.

Hedges that saved Lehman Brothers billons early this year either failed to work

during the second quarter, leaving the firm to take its losses, or worked

against it, meaning the bank lost money both on the value of the assets and the

hedges.

For example, in the first quarter, Lehman’s gross mark-to-market adjustments —

the write-downs the firm faced in light of declining asset values — totaled $4.7

billion. But hedges on residential mortgages and commercial mortgage-related

positions allowed the firm to post net write-downs of only $1.8 billion.

In the most recent quarter, the net write-down was $3.7 billion — more than the

gross write-down of $3.6 billion. The worst-performing hedge was on commercial

mortgage-related positions: asset values lost $700 million but ineffective

hedging resulted in a total net write-down of $1.1 billion (in the first quarter

the gross write-down was $1.1 billion and the net only $700 million).

On Monday’s conference call, Ms. Callan said counterparties to Lehman’s trades

were not pulling out, refuting statements by others that Lehman might lose money

in the quarter because of some of its trading partners back out.

Last Thursday, Brad Hintz, the banking analyst at Sanford Bernstein and former

chief financial officer at Lehman, lowered his estimate for Lehman’s third- and

fourth-quarter earnings each by 11 cents per share, writing: “Confidence

concerns about any broker will have a negative impact on the firm’s bottom line.

Fixed-income counterparties become more discerning about which LEH subsidiaries

they will trade with.”

When analysts asked Ms. Callan about its hard-to-value assets, known as Level 3

assets, she said she could not say whether they would be down this quarter. She

said some assets would move to Level 3 categorization this quarter.

William F. Tanona, an analyst at Goldman Sachs, predicted that Lehman’s stock

would fall as investors digested the unexpected loss, but would recover as the

day wore on as short sellers covered their positions.

“Today’s results were far worse than anyone had anticipated,” he wrote. “Results

were plagued by continued write-downs and ineffective hedges.”

Lehman Posts Loss and Plans to Raise Capital, NYT,

10.6.2008,

http://www.nytimes.com/2008/06/10/business/10lehman.html?hp

Dow

Rebounds as Oil Prices Decline

June 10,

2008

The New York Times

By ABHA BHATTARAI

Oil prices

retreated in volatile trading on Monday, helping the Dow Jones industrial

average bounce back from its big losses on Friday. But a larger-than-expected

loss from Lehman Brothers added to continued concerns about credit markets.

The Dow Jones industrial average, which took its biggest hit in 15 months on

Friday, was up 89.48, or 0.7 percent, to 12,299.29, at 12:30 p.m.

The Standard & Poor’s 500-stock index gained 0.4 percent, while the Nasdaq

composite index, after opening slightly higher, was down 0.7 percent.

More upbeat news came Monday with an unexpected increase in pending home sales

in April. The National Association of Realtors reported the highest reading in

the index since October, though it remains more than 13 percent below a year

ago.

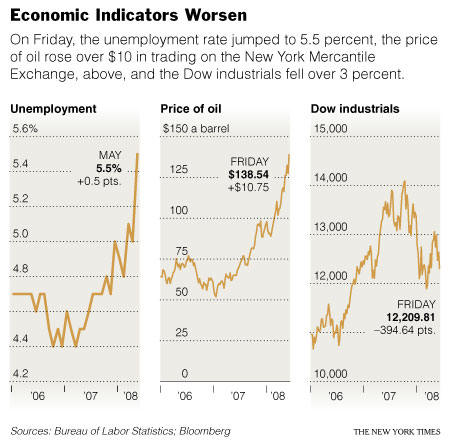

A record one-day surge in the price of oil on Friday, to more than $138 a

barrel, helped send markets into a tailspin. The three main indexes were down 3

percent or more, with the Dow dropping almost 400 points.

Analysts said the stock market’s slight gains on Monday were not cause for

celebration.

“If you take a cat and throw it off the top of a building, it’ll bounce off the

street but that doesn’t mean it’s alive,” said Marc Chandler, who oversees

currency strategy at Brown Brothers Harriman. “This is partly a dead cat bounce,

and it’s partly because investors are thinking Friday went too far too fast.”

Investors were keeping an eye on oil prices, which pulled back on Monday. West

Texas intermediate crude for July delivery was down $3 shortly after 10 a.m.,

then recovered most of those losses before heading down again. At 11 a.m., it

was at $136.80, down $1.74.

Bruce Bittles, an investment strategist at Robert W. Baird & Company, said the

drop in oil prices was “not significant.”

“What’s happening right now is to be expected after Friday’s brutal beating,” he

said. “I don’t think you can read too much into the action right now.”

Traders were also watching Lehman Brothers, which announced an unexpected $2.8

billion loss and said it planned to raise $6 billion in capital. Its shares were

down about 9 percent, to $29.40, at loss of $2.89, shortly after noon. They are

down more than 50 percent this year.

Dow Rebounds as Oil Prices Decline, NYT, 10.6.2008,

http://www.nytimes.com/2008/06/10/business/10stox.html

Bush

says strong dollar in U.S. interest

Mon Jun 9,

2008

9:43am EDT

Reuters

By Tabassum Zakaria

WASHINGTON

(Reuters) - U.S. President George W. Bush acknowledged economic concerns as he

left for Europe on Monday, saying the United States was committed to a strong

dollar and that energy prices were high.

"I'll talk about our nation's commitment to a strong dollar. A strong dollar is

in our nation's interests. It is in the interests of the global economy," Bush

said at the White House before departing for a U.S.-European Union summit in

Slovenia.

The dollar tumbled on Friday after a jump in the unemployment rate underscored

the U.S. economy's weakness and was a factor that contributed to the biggest

one-day price gain in the history of the oil market. Oil surged by nearly $11 a

barrel to a record above $139.

Europeans are concerned about the dollar's weakness and have urged the Bush

administration to speak up more forcefully in defense of the U.S. currency.

Since oil is priced in dollars, Europeans blame some of their inflation

pressures on the dollar's weakening value and fear the cheap dollar will make

their products more expensive in U.S. consumer markets.

Bush will discuss the economy with European leaders during his June 9-16 trip,

which will include stops in Germany, Italy, France and Britain.

"Our economy is large and it's open and flexible," Bush said. "Our capital

markets are some of the deepest and most liquid. And the long-term health and

strong foundation of our economy will shine through and be reflected in currency

values."

He said he recognized the public was concerned about the U.S. economy in the

face of rising energy prices.

"A lot of Americans are concerned about our economy," Bush said. "I can

understand why. Gasoline prices are high, energy prices are high."

He said he would discuss with European allies the need to advance technologies

to become less dependent on hydrocarbons. Bush reiterated his stance that the

United States should increase domestic oil production and that Congress should

allow drilling in Alaska's Arctic National Wildlife Refuge.

Record-high oil prices have raised concerns about the impact on the U.S.

economy, which is barely growing. The U.S. unemployment rate jumped to 5.5

percent in May, its highest in more than 3-1/2 years, contributing to renewed

fears that the U.S. economy was at risk of sliding into recession.

"The U.S. economy has continued to grow in the face of unprecedented

challenges," Bush said.

"We got to keep our economies flexible. Both the U.S. economy and European

economies need to be flexible in order to deal with today's challenges," he

said.

Bush said he also would discuss with European allies the need to do more to help

Afghanistan. His wife, Laura, visited Afghanistan during the weekend and

reported that she saw progress but also "there's a lot of work to be done," Bush

said.

(Editing by Bill Trott)

Bush says strong dollar in U.S. interest, R, 9.6.2008,

http://www.reuters.com/article/politicsNews/idUSN0944596220080609

EYES ON THE

ROAD

By JOSEPH

B. WHITE

Top Car

Dealer Says High Gas Prices Are Good for the U.S. Auto Industry

AutoNation

CEO Says Increase Will Drive Demand For Hybrids, Electric Cars and Other

Alternatives

June 9,

2008

The Wall Street Journal

Detroit's

big auto makers are slashing jobs, closing factories and undertaking costly

revamps of their product strategies to cope with $4 a gallon gas. What's the

worst thing that could happen now? Gas could get cheap again, says the man who

runs America's biggest auto retailer.

"For once we actually have viable alternatives and exciting technology that are

really game changers" in the effort to wean transportation from petroleum, says

Mike Jackson, chairman and chief executive officer of AutoNation Inc. "However,

if the price of petroleum goes down … it undercuts the viability of new

technology."

"You have to tell the American people the truth," he says. "Energy costs will be

higher."

It might seem odd that America's leading car salesman would want gasoline prices

to stay high, given how much damage the recent surge in pump prices has done to

demand for the big sport-utility vehicles and pickups that once powered sales at

many AutoNation stores.

But Mr. Jackson's point of view about energy policy and the auto industry isn't

based on concerns about this month's sales. What has him worried, he says, is

that in the future he -- and by extension the whole auto industry -- will be

stuck trying to make sense of a fundamentally incoherent national energy

strategy, which was mirrored by the seemingly incoherent product strategies that

the big U.S. auto makers were pursuing until $130 a barrel oil blew them up.

Readers,

over to you: If you had a big SUV or pickup would you be getting rid of it now?

Discuss.Mr. Jackson confronts a daunting challenge trying to read American

culture and make intelligent bets about what consumers will want to drive.

If he looks in one direction, he sees a widespread consensus that, for a

combination of environmental and national security reasons, Americans should

consume less oil. To that end, Americans want the auto industry to speed

production of electric vehicles and high-mileage, gasoline-electric hybrids,

while substantially improving the mileage of conventional oil-powered cars.

Here's the big news: The auto industry finally appears willing and eager to

respond.

It's

entirely possible that a decade from now, we'll realize that this was a pivotal

moment in the auto industry's history. This could be the moment when a century

of relying almost exclusively on petroleum to power personal mobility gives way

to a new model, in which electricity powers our transportation.

Indeed, there's a case that consumers who want to buy into the next generation

of transportation technology shouldn't buy a new car until 2010 or 2011. By

then, General Motors Corp. has promised to deliver its hybrid-electric Chevrolet

Volt; Nissan Motor Corp. has said it will begin offering electric cars; Honda

Motor Co. and several European manufacturers have promised to launch in the U.S.

new, advanced, high-mileage clean diesel cars; and Toyota Motor Corp. might have

a whole family of hybrid vehicles based on the next generation Toyota Prius.

A gaggle of small companies such as Norway's Think Global AS and Silicon

Valley's Tesla Motors Inc. are all gearing up to expand the electric vehicle

market if the big guys won't. But the excitement over projects like the Tesla

Roadster can't compare to the significance of the shift in mindset among the

people who run the world's biggest auto companies. This isn't a crowd given to

green idealism, but they have come to the conclusion that remaining totally

shackled to petroleum is bad for business and are re-gearing their future

vehicle plans accordingly.

But when

Mr. Jackson looks in the other direction he sees a widespread consensus that

Americans shouldn't have to pay $4 a gallon or more for gasoline, and a Congress

that in an election year has put driving down gas prices at the top of its

agenda.

Further, he confronts the inertia of more than half a century of automotive

marketing investment in teaching consumers that size and power are what make a

vehicle desirable, and worth more money.

Mr. Jackson, like others of his baby boom generation, remembers well what

happened in the 1980s, after the last big oil price shock. Through a combination

of conservation and new production, the U.S. turned the tables on the oil

producers. Gas prices plunged, sales of gas guzzlers took off and the table was

set for the crisis the U.S. auto industry faces today.

"We are highly skilled at selling size, horsepower and speed at a premium price,

and giving away fuel efficiency," Mr. Jackson says. "Now, going forward over the

next 10 years we are going to have to convince consumers why they should pay

more for a smaller engine…or some new technology that is going to give them a

tremendous benefit on fuel efficiency. That's a completely new world for us."

"I'm a good car salesman," Mr. Jackson says. "If I have high gas prices and an

open-minded consumer, it's very doable. There is a connection between their

needs and what we have to offer them. If we have cheap gasoline, it's mission

impossible."

Top Car Dealer Says High Gas Prices Are Good for the U.S.

Auto Industry, WSJ, 9.6.2008,

http://online.wsj.com/article/SB121276760051852173.html?mod=hpp_us_inside_today

Rural

U.S. Takes Worst Hit as Gas Tops $4 Average

June 9,

2008

The New York Times

By CLIFFORD KRAUSS

TCHULA,

Miss. — Gasoline prices reached a national average of $4 a gallon for the first

time over the weekend, adding more strain to motorists across the country.

But the pain is not being felt uniformly. Across broad swaths of the South,

Southwest and the upper Great Plains, the combination of low incomes, high gas

prices and heavy dependence on pickup trucks and vans is putting an even tighter

squeeze on family budgets.

Here in the Mississippi Delta, some farm workers are borrowing money from their

bosses so they can fill their tanks and get to work. Some are switching jobs for

shorter commutes.

People are giving up meat so they can buy fuel. Gasoline theft is rising. And

drivers are running out of gas more often, leaving their cars by the side of the

road until they can scrape together gas money.

The disparity between rural America and the rest of the country is a matter of

simple home economics. Nationwide, Americans are now spending about 4 percent of

their take-home income on gasoline. By contrast, in some counties in the

Mississippi Delta, that figure has surpassed 13 percent.

As a result, gasoline expenses are rivaling what families spend on food and

housing.

“This crisis really impacts those who are at the economic margins of society,

mostly in the rural areas and particularly parts of the Southeast,” said Fred

Rozell, retail pricing director at the Oil Price Information Service, a fuel

analysis firm. “These are people who have to decide between food and

transportation.”

A survey by Mr. Rozell’s firm late last month found that the gasoline crisis is

taking the highest toll, as a percentage of income, on people in rural areas of

the South, New Mexico, Montana, Wyoming and North and South Dakota.

With the exception of rural Maine, the Northeast appears least affected by

gasoline prices because people there make more money and drive shorter

distances, or they take a bus or train to work.

But across Mississippi and the rural South, little public transit is available

and people have no choice but to drive to work. Since jobs are scarce, commutes

are frequently 20 miles or more. Many of the vehicles on the roads here are old

rundown trucks, some getting 10 or fewer miles to the gallon.

The survey showed that of the 13 counties where people spent 13 percent or more

of their family income on gasoline, 5 were located in Mississippi, 4 were in

Alabama, 3 were in Kentucky and 1 was in West Virginia. While people here in

Holmes County spent an average of 15.6 percent of their income on gasoline,

people in Nassau County, N.Y., spent barely more than 2 percent, according to

the survey.

Economists say that despite widespread concern about gasoline prices, the

nationwide impact of the oil crisis has so far been gentler than during the oil

crises of the 1970s and 1980s, when shortages caused long lines at the pump, set

off inflation and drove the economy into recession.

Americans on average now spend about 4 percent of their after-tax income on

transportation fuels, according to Brian A. Bethune, an economist at Global

Insight, a forecasting firm. That compares with 4.5 percent in early 1981, the

highest point since World War II. At its lowest point, in 1998, that share

dropped to 1.9 percent.

“Gas prices have doubled over the last year but the economy has not fallen off

the cliff,” said Rajeev Dhawan, director of the Economic Forecasting Center at

Georgia State University. “But for the rural lower income people, as a

proportion of their income the rise of gas prices is very high.”

While people everywhere are talking about gasoline prices these days, some folks

in Tchula (the T is silent) have gone beyond talking.

Anthony Clark, a farm worker from Tchula, says he prays every night for lower

gasoline prices. He recently decided not to fix his broken 1992 Chevrolet Astro

van because he could not afford the fuel. Now he hires friends and family

members to drive him around to buy food and medicine for his diabetic aunt, and

his boss sends a van to pick him up for the 10-mile commute to work.

A trip from Tchula to the nearest sizable town about 15 minutes away can cost

him $25 roundtrip — for the driving and the waiting. That is about 10 percent of

what he makes in a week.

Taking a break under some cottonwood trees beside a drainage ditch filled with

buzzing mosquitoes, Mr. Clark and members of his work crew spoke of the big and

little changes that higher gas prices have brought. The extra dollars spent at

the pump mean electric bills are going unpaid and macaroni is replacing meat at

supper. Donations to church are being put off, and video rentals are now

unaffordable.

Cleveland Whiteside, who works with Mr. Clark and used to commute 30 miles a

day, said his Jeep Cherokee was repossessed last month, because “I paid so much

for gas to get to work I couldn’t pay my payments anymore.” His employer, Larry

Clanton, has lent him a pickup truck so he can get to work.

Signs of pain and adaptation because of the cost of gas are everywhere. Local

fried chicken restaurants are closing because people are eating out less. At the

hardware store here, sales have plummeted to $30 a day from $250 a day a month

ago.

“Money goes to gasoline — I know mine does,” said the hardware store’s manager,

Pam Williams, who tries to attract customers by putting out choice crickets for

fishing bait beside the front door.

Local governments are leaving grass high along the roads and doing fewer road

repairs to save on fuel costs. The Holmes County government has cut the work

week to four days to give workers gasoline relief (keeping the same total of

hours), and politicians are even considering replacing sanitation workers with

prison inmates on some shifts to conserve money for fuel.

The local price for a gallon of regular unleaded gasoline was roughly $3.85 last

week, slightly below the national average, but the median family income in

Holmes County is about $18,500.

Nationwide, regular unleaded gasoline reached an average of $4.005 on Sunday,

according to the American Automobile Association. That is the highest price ever

and about a dollar higher than at the start of the year.

While looking to cut workers at his fish processing plant in nearby Isola,

Miss., Dick Stevens, president of Consolidated Catfish Producers, said that 10

workers walked into his office last week and volunteered to take a buyout rather

than continue commuting from Charleston, Miss., 65 miles away. “The gas ate them

alive,” he said.

Workers at the plant are trying to find ways to cope. Josephine Cage, who

fillets fish, said her 30-mile commute from Tchula to Isola in her 1998 Ford

Escort four days a week is costing her $200 a month, or nearly 20 percent of her

pay.

“I make it by the grace of God,” she said, and also by replacing meat at supper

with soups and green beans and broccoli. She fills her car a little bit every

day, because “I can’t afford to fill it up. Whatever money I have, I put it in.”

Sociologists and economists who study rural poverty say the gasoline crisis in

the rural South, if it persists, could accelerate population loss and decrease

the tax base in some areas as more people move closer to urban manufacturing

jobs. They warn that the high cost of driving makes low-wage labor even less