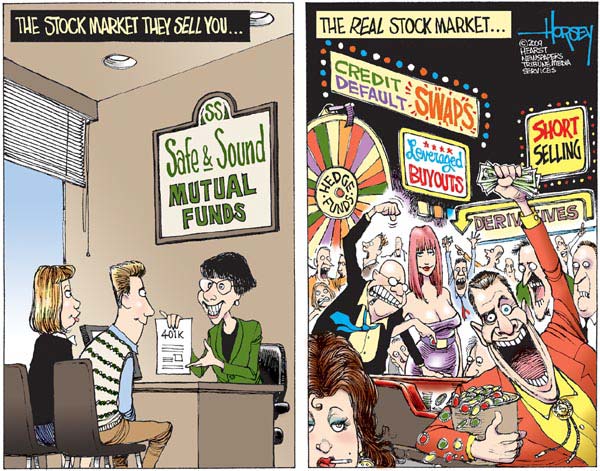

THE stock

market has been big news in recent days. Last week’s report that Deutsche Börse,

a giant German exchange, intends to buy the New York Stock Exchange, creating a

company worth some $24 billion, arrived shortly after the Dow broke the

12,000-point barrier for the first time since before the financial crisis.

These developments drew headlines because they seemed to exemplify significant

trends in the American economy. But look at America’s stock exchanges more

closely, and there’s less to them than meets the eye. In truth, the stock market

is becoming increasingly irrelevant — a trend that threatens the core principles

of American capitalism.

These days a healthy stock market doesn’t mean a healthy economy, as a glance at

the high unemployment rate or the low labor-market participation rate will show.

The Tea Party is right about one thing: What’s good for Wall Street isn’t

necessarily good for Main Street. And the Germans aren’t buying the New York

Stock Exchange for its commoditized, highly competitive and ultra-low-margin

stock business, but rather for its lucrative derivatives operations.

The stock market is still huge, of course: the companies listed on American

exchanges are valued at more than $17 trillion, and they’re not going to

disappear in the foreseeable future.

But the glory days of publicly traded companies dominating the American business

landscape may be over. The number of companies listed on the major domestic

exchanges peaked in 1997 at more than 7,000, and it has been falling ever since.

It’s now down to about 4,000 companies, and given its steep downward trend will

surely continue to shrink.

Nor are the remaining stocks an obvious proxy for the health of the American

economy. Innovative American companies like Apple and Google may be worth

hundreds of billions of dollars, but most of them don’t pay dividends or employ

many Americans, and their shares are essentially speculative investments for

people making a bet on how we’re going to live in the future.

Put another way, as the number of initial public offerings steadily declines,

the stock market is becoming little more than a place for speculators and

algorithms to compete over who can trade his way to the most money.

What the market is not doing so well is its core public function: allocating

capital efficiently. Apple, for instance, is hugely profitable and sits on an

enormous pile of cash; it is thus very unlikely to use its highly rated stock to

pay for any acquisitions. It hasn’t used the stock market to raise money since

1981, and there’s a good bet it never will again.

Meanwhile, the companies in which people most want to invest, technology stars

like Facebook and Twitter, are managing to avoid the public markets entirely by

raising hundreds of millions or even billions of dollars privately. You and I

can’t buy into these companies; only very select institutions and well-connected

individuals can. And companies prefer it that way.

A private company’s stock isn’t affected by the unpredictable waves of the stock

market as a whole. Its chief executive can concentrate on running the company

rather than answering endless questions from investors, analysts and the press.

There’s much less pressure to meet quarterly earnings targets. When the stock

does trade, the deals can be negotiated quietly, in private markets, rather than

fall victim to short-term speculation from the high-frequency traders who

populate public markets. And companies love how private markets allow them to

avoid much of the regulatory burden of being public.

That burden comes largely from the Securities and Exchange Commission, which was

created in the wake of the 1929 stock-market crash to protect small investors.

But if the move to private markets continues, small investors aren’t going to

need much protection any more: they’ll be able to invest in only a relative

handful of companies anyway.

Only the biggest and oldest companies are happy being listed on public markets

today. As a result, the stock market as a whole increasingly fails to reflect

the vibrancy and heterogeneity of the broader economy. To invest in younger,

smaller companies, you increasingly need to be a member of the ultra-rich elite.

At risk, then, is the shareholder democracy that America forged, slowly, over

the past 50 years. Civilians, rather than plutocrats, controlled corporate

America, and that relationship improved standards of living and usually kept the

worst of corporate abuses in check. With America Inc. owned by its citizens, the

success of American business translated into large gains in the stock portfolios

of anybody who put his savings in the market over most of the postwar period.

Today, however, stock markets, once the bedrock of American capitalism, are

slowly becoming a noisy sideshow that churns out increasingly meager returns.

The show still gets lots of attention, but the real business of the global

economy is inexorably leaving the stock market — and the vast majority of us —

behind.

When the

financial crisis struck, many people — myself included — considered it a

teachable moment. Above all, we expected the crisis to remind everyone why banks

need to be effectively regulated.

How naïve we were. We should have realized that the modern Republican Party is

utterly dedicated to the Reaganite slogan that government is always the problem,

never the solution. And, therefore, we should have realized that party

loyalists, confronted with facts that don’t fit the slogan, would adjust the

facts.

Which brings me to the case of the collapsing crisis commission.

The bipartisan Financial Crisis Inquiry Commission was established by law to

“examine the causes, domestic and global, of the current financial and economic

crisis in the United States.” The hope was that it would be a modern version of

the Pecora investigation of the 1930s, which documented Wall Street abuses and

helped pave the way for financial reform.

Instead, however, the commission has broken down along partisan lines, unable to

agree on even the most basic points.

It’s not as if the story of the crisis is particularly obscure. First, there was

a widely spread housing bubble, not just in the United States, but in Ireland,

Spain, and other countries as well. This bubble was inflated by irresponsible

lending, made possible both by bank deregulation and the failure to extend

regulation to “shadow banks,” which weren’t covered by traditional regulation

but nonetheless engaged in banking activities and created bank-type risks.

Then the bubble burst, with hugely disruptive consequences. It turned out that

Wall Street had created a web of interconnection nobody understood, so that the

failure of Lehman Brothers, a medium-size investment bank, could threaten to

take down the whole world financial system.

It’s a straightforward story, but a story that the Republican members of the

commission don’t want told. Literally.

Last week, reports Shahien Nasiripour of The Huffington Post, all four

Republicans on the commission voted to exclude the following terms from the

report: “deregulation,” “shadow banking,” “interconnection,” and, yes, “Wall

Street.”

When Democratic members refused to go along with this insistence that the story

of Hamlet be told without the prince, the Republicans went ahead and issued

their own report, which did, indeed, avoid using any of the banned terms.

That report is all of nine pages long, with few facts and hardly any numbers.

Beyond that, it tells a story that has been widely and repeatedly debunked —

without responding at all to the debunkers.

In the world according to the G.O.P. commissioners, it’s all the fault of

government do-gooders, who used various levers — especially Fannie Mae and

Freddie Mac, the government-sponsored loan-guarantee agencies — to promote loans

to low-income borrowers. Wall Street — I mean, the private sector — erred only

to the extent that it got suckered into going along with this government-created

bubble.

It’s hard to overstate how wrongheaded all of this is. For one thing, as I’ve

already noted, the housing bubble was international — and Fannie and Freddie

weren’t guaranteeing mortgages in Latvia. Nor were they guaranteeing loans in

commercial real estate, which also experienced a huge bubble.

Beyond that, the timing shows that private players weren’t suckered into a

government-created bubble. It was the other way around. During the peak years of

housing inflation, Fannie and Freddie were pushed to the sidelines; they only

got into dubious lending late in the game, as they tried to regain market share.

But the G.O.P. commissioners are just doing their job, which is to sustain the

conservative narrative. And a narrative that absolves the banks of any

wrongdoing, that places all the blame on meddling politicians, is especially

important now that Republicans are about to take over the House.

Last week, Spencer Bachus, the incoming G.O.P. chairman of the House Financial

Services Committee, told The Birmingham News that “in Washington, the view is

that the banks are to be regulated, and my view is that Washington and the

regulators are there to serve the banks.”

He later tried to walk the remark back, but there’s no question that he and his

colleagues will do everything they can to block effective regulation of the

people and institutions responsible for the economic nightmare of recent years.

So they need a cover story saying that it was all the government’s fault.

In the end, those of us who expected the crisis to provide a teachable moment

were right, but not in the way we expected. Never mind relearning the case for

bank regulation; what we learned, instead, is what happens when an ideology

backed by vast wealth and immense power confronts inconvenient facts. And the

answer is, the facts lose.

• FTSE 100 down 2%; Dow loses 1%

• Euro slides to two-month low against US dollar

• Cost of insuring Spanish and Portuguese debt

hits record high

Monday 29 November 2010

19.35 GMT

Guardian.co.uk

Jill Treanor and Julia Kollewe

This article was published

on guardian.co.uk at 19.35 GMT

on Monday 29 November

2010.

A version appeared

on p28 of the Main section section

of the Guardian on Tuesday

30 November 2010.

It was last modified

at 01.30 GMT on Tuesday 30 November 2010.

It was first

published

at 10.40 GMT on Monday 29 November 2010.

Stocks fell on both sides of the Atlantic, the euro tumbled, and the cost of

borrowing for Ireland, Spain and Portugal jumped today, as details of the

republic's €85bn (£72bn) bailout failed to quell anxiety that the crisis in the

eurozone was deepening.

Amid speculation that the European authorities may be left with little option

but to embark on large-scale quantitative easing to try to bolster sentiment,

Ireland's borrowing costs shot as high as 9.6% as the terms of its bailout by

the International Monetary Fund and European Union were digested by investors.

"The bottom line is that the financial markets are unimpressed, and that's the

most generous description," Neil MacKinnon, global macro strategist at VTB

Capital told Associated Press. "The crisis rumbles on."

Only two shares in the FTSE 100, Barclays and HSBC, ended the day in positive

territory as the blue-chip index closed below 5600 for the first time since 1

October, down 2% at 5550.

The Dow Jones industrial average fell 39.51 points to 11,052.49, and the euro

slid to a new two-month low against the dollar of $1.3065 amid concerns about

the long-term future of the decade-old single currency.

The cost of borrowing for the peripheral eurozone countries stayed stubbornly

high, with Portugual above 7% and Spain above 5%, as speculation focused on the

next indebted country which might need financial help. Italy endured its biggest

one day rise in borrowing costs for a decade.

The cost of insuring Portuguese debt against default rose to a record high after

Nouriel Roubini, economics professor and chairman of Roubini Global Economics,

urged Lisbon to take international assistance. "Like it or not, Portugal is

reaching the critical point," Roubini told the Portuguese newspaper Diário

Económico. "Perhaps it could be a good idea to ask for a bailout in a

preventative manner."

Ireland's bailout failed to dent fears of contagion across the eurozone despite

rallying cries by France's economy minister Christine Lagarde and Germany's

finance minister Wolfgang Schäuble, who both insisted Portugal would not need

help. Andrew Lim, head of financials research at Matrix investment bank, said:

"The Irish bailout doesn't solve the euro problem … We are looking at Portugal,

then Spain next."

The fragility in the markets led to speculation that the European Central Bank

will delay attempts to begin withdrawing funds for banks at its meeting on

Thursday, even though the €35bn earmarked for Ireland's banks was intended to

wean them off the ECB's life support.

Analysts said although the Ireland bailout had been accompanied by plans for new

ways to rescue troubled eurozone countries after 2013, when the current

emergency schemes run out, investors had been left confused. It was still not

clear in what circumstances bondholders would be expected to share the losses of

countries that were allowed to reschedule their debt after 2013 – in effect

defaulting.

"Given the lack of clarity about what constitutes the appearance of insolvency,

and what type of restructuring might occur in such a case, markets are likely to

remain wary of holding government debt issued by other troubled eurozone

countries like Portugal and Spain," said Ben May, European economist at Capital

Economics.

"With huge political frictions still clearly in place within the region, fears

of a future break-up of the region look set to remain, placing further downward

pressure on the euro."

The bailout for Ireland is intended to ensure that neither the country nor its

banks will default on their debt. The decision by the authorities to ensure that

the possibility of default was reduced was initially welcomed. Gary Jenkins,

head of fixed income research at Evolution Securities, said: "This is not the

time to inject panic into the banking sector."

Greece, the first eurozone country to be bailed out, was today given until 2021

to repay its €110bn loan from the IMF and EU, rather than 2015.

Greece's finance minister George Papaconstantinou said: "We have a grace period

of four years and a repayment period of seven years.

"The decision is very important, it opens the way to return to markets earlier

than expected."

September 19, 2010

The New York Times

By NELSON D. SCHWARTZ

Inside the great investment houses on Wall Street, business has taken a

surprising turn — downward.

Even after taxpayer bailouts restored bankers’ profits and pay, the great Wall

Street money machine is decelerating. Big financial institutions, including

commercial banks, are still making a lot of money. But given unease in the

financial markets and the economy, brokerages and investment banks are not

making nearly as much as their executives, employees and investors had hoped.

After an unusually sharp slowdown in trading this summer, analysts are

rethinking their profit forecasts for 2010.

The activities at the heart of what Wall Street does — selling and trading

stocks and bonds, and advising on mergers — are running at levels well below

where they were at this point last year, said Meredith Whitney, a bank analyst

who was among the first to warn of the subprime mortgage disaster and its impact

on big banks.

Worldwide, the number of stock offerings is down 15 percent from this time last

year, while bond issuance is off 25 percent, according to Capital IQ, a research

firm. Based on these trends, Ms. Whitney predicts that annual revenue from Wall

Street’s main businesses will drop 25 percent, to around $42 billion in 2010,

from $56 billion last year.

While the numbers will not be known until after the third quarter ends and

financial companies begin reporting earnings in October, the pace of trading

this summer was slow even by normal summer standards. Trading in shares listed

on the New York Stock Exchange was down by 11 percent in July from 2009 levels,

and August volume was off nearly 30 percent.

“What’s happened in the third quarter is that after a very slow summer, people

expected things to come back,” said Ms. Whitney. “But they haven’t, and the

inactivity is really squeezing everyone.”

The downward slide on Wall Street parallels a similar shift in the broader

economy, which has slowed considerably since showing signs of a nascent recovery

this spring. And if banks come under pressure, all but the safest borrowers may

struggle to get loans.

With less than two weeks to go in the third quarter, companies will be

hard-pressed to fulfill earlier, more optimistic expectations.

“It’s like the marathon: if you’re five miles behind, you can’t make that up in

the last 10 minutes of the race,” said David H. Ellison, president of FBR Fund

Advisers, a money management firm that specializes in financial companies. Many

banks are barely scraping by in traditional Wall Street business.

As a result, executives, portfolio managers and analysts say that even the

mighty Goldman Sachs, which posted a profit every day for the first three months

of the year, is unlikely to deliver the kind of profit growth that investors

have come to expect.

Keith Horowitz, a bank analyst at Citigroup, said he expected Goldman Sachs to

earn $7.8 billion in 2010, a 35 percent decline from the $12.1 billion it made

last year.

The drop in trading translates into lower commissions for brokerage firms, as

well as a weaker environment for underwriting initial public offerings and other

stock issues, traditionally a highly lucrative niche.

Banks are also scaling back on making bets with their own money — known as

proprietary trading — another huge profit source in recent years that will soon

be forbidden under terms of the financial reform legislation passed by Congress

this summer.

Indeed, analysts have finally started to bring their forecasts in line with the

new reality. On Sept. 12, Mr. Horowitz reduced his estimates for third-quarter

profits at Goldman and Morgan Stanley.

Mr. Horowitz had predicted Goldman would make $1.75 billion in the third

quarter, or $3 a share; he now expects Goldman’s profit to total $1.34 billion,

or $2.30 a share. For Morgan Stanley, his revision was even steeper, with

earnings expectations revised downward to $140 million, or 10 cents a share,

from $726 million, or 53 cents a share.

Mr. Horowitz’s estimates are considerably lower than the consensus among

analysts who track the two companies. If the other analysts revise their

estimates closer to his, they would put pressure on the shares.

One of the rare bright spots for Wall Street recently has been the issuance of

junk bonds, as ultra-low interest rates encourage investors to seek out riskier

debt that carries a higher yield. But that will not be enough to offset the

weakness elsewhere, said one top Wall Street executive who insisted on anonymity

because he was not authorized to speak publicly for his company, and because

final numbers would not be tallied until the end of the month.

To make matters worse, he said, many Wall Street firms increased their work

forces in the first half of the year, before the mood shifted and worries of a

double-dip recession arose. If activity remains anemic, firms could soon begin

cutting jobs again.

“I think the summer was horrible for everyone, and no one expected it to be as

bad as it was,” he said. “It’s coming back a little bit in September but nowhere

near enough to make up for what happened in July and August.”

The profit picture is brighter for diversified companies like JPMorgan Chase and

Bank of America, which have larger commercial and retail banking operations in

addition to their Wall Street units, but some analysts say earnings expectations

for them could come down as well.

“Estimates still seem a little high, and the revenue story for all the banks is

not a good one,” said Ed Najarian, who tracks the banking sector for ISI, a New

York research firm.

With interest rates plunging, banks are making less off their interest-earning

assets like government bonds and other ultra-safe securities. At the same time,

demand for new loans remains weak.

One wild card will be the credit card portfolios at major banks like JPMorgan,

Bank of America and Citigroup. As delinquencies ease, Mr. Najarian said, credit

losses are likely to decline. That trend helped earnings at JPMorgan in the

second quarter, and could be crucial again in the third quarter.

Ms. Whitney says the gloomy short-term predictions foreshadow a series of lean

years in the broader financial services industry.

Indeed, she said the Street faced a “resizing” not seen since the cutbacks that

followed the bursting of the dot-com bubble a decade ago.

“We expect compensation to be down dramatically this year,” she wrote in a

recent report. She predicts the American banking industry will lay off 40,000 to

80,00 employees, or as many as 1 in 10 of its workers.

That may be extreme, but Ms. Whitney argues that the boom years are not coming

back anytime soon. As both consumers and companies cut back on debt, and

financial reform rules put the brakes on profitable niches like derivatives and

proprietary trading, the engines of earnings growth for the last decade will

continue to sputter.

There is much to applaud in the financial regulatory reform bill announced

last Friday by House and Senate negotiators. It would limit some of the riskiest

activities of banks and regulate the multitrillion-dollar market in

over-the-counter derivatives. It would give federal regulators the tools, if

they need them, to shut failing large banks and financial firms instead of

bailing them out.

In significant ways, the bill would also protect Americans directly. Consumers

would be shielded from many forms of abusive and predatory lending, and

investors could be empowered to influence corporate boards that have long been

impervious to shareholder concerns.

The bill is a considerable accomplishment. It is the final version. Congress

should pass it quickly.

At the same time — and in the months and years ahead — lawmakers must

acknowledge the bill’s shortcomings and be prepared to take corrective action.

Many of the bill’s provisions come with exceptions or exemptions that could, in

practice, swallow the new rules.

The reforms are also vulnerable to being weakened in the painstaking process of

translating new law into actual regulations and procedures. Special interests —

think Wall Street — have the resources and time to monitor and influence that

process. The public does not. Lawmakers have to ensure the carrying out of the

rules does not veer widely from what Congress has promised.

Take for example, the so-called Volcker rule, intended to reduce risk and

speculation in the financial system. The Obama administration proposed banning

banks from using their capital to invest in hedge funds and private equity

funds. The final bill would let banks invest up to 3 percent of their

high-quality capital in such funds, a big exception. Congress has to be prepared

to reduce the percentage to control risks in the system.

Derivatives regulation also bears watching. The bill would require most

transactions to occur on regulated exchanges, rather than as private contracts.

Regulators and lawmakers must strictly monitor derivatives that trade

off-exchange and stop that market from growing ever larger.

For all of the specific reforms, the legislation leaves intact a handful of

behemoth, multitasking banks whose size and scope would make them difficult to

dismantle in a crisis, even under a new law.

Congress is gambling that the reforms, taken together, will sufficiently reduce

the banks’ riskiness. That could happen, but if it does, the banks will make

considerably less money and will want relief from what they are sure to call

overly burdensome regulation. When that happens — and if the reforms work, it

will — lawmakers will have to stand firm, even though it means imposing pain on

the banks. Equally important, if the big banks grow larger and riskier despite

the new rules, will lawmakers impose stronger restraints? If they do not, it is

only a matter of time before the next calamity.

Americans have paid for the financial crisis with their jobs, incomes, savings,

investments and home equity, and with their faith in markets and in the

government to protect them from harm. The new bill is a step toward redressing

those losses and restoring that faith. Congress should pass it, and then do what

must be done to ensure that it performs as advertised.

June 25, 2010

The New York Times

By EDWARD WYATT

and DAVID M. HERSZENHORN

WASHINGTON — An overhaul of the nation’s financial regulatory system, reached

after an all-night Congressional horse-trading session, will vastly expand the

authority of the federal government over Wall Street in a bid to curb the

free-wheeling culture that led to the near collapse of the world economy in

2008.

The deal between House and Senate negotiators, sealed just before sunrise on

Friday, imposes new rules on some of the riskiest business practices and exotic

investment instruments. It also levies hefty fees on the financial services

industry, essentially forcing big banks and hedge funds to pay the projected $20

billion, five-year cost of the new oversight that they will face. And it

empowers regulators to liquidate failing financial companies, fundamentally

altering the balance between government and industry.

But after weeks of intense lobbying and months of debate, Congress in the end

stopped short of prohibiting some of the practices that led to the crisis two

years ago, betting instead that a newly empowered regulatory regime can rein in

the big financial players without shackling the markets and drying up the flow

of credit to businesses.

“We are poised to pass the toughest financial reform since the ones we created

in the aftermath of the Great Depression,” President Obama said on the South

Lawn of the White House, before leaving for the Group of 20 meeting in Toronto,

where he was expected to press other nations to tighten their financial rules.

Democrats predicted that the full Congress would approve the legislation next

week and that they would meet their goal of sending the bill to Mr. Obama for

his signature by the Fourth of July.

The financial industry won some important victories, even if they face

significantly heightened regulation. They fought off some of the toughest

restrictions on their ability to invest their own funds. Most significantly,

they thwarted an attempt to make them give up their highly profitable

derivatives trading desks. And big lobbying fights remain in the future, when

regulators begin the nitty-gritty task of turning complex, sometimes vague laws

into real-world rules for these businesses to follow.

Industry analysts predicted that banks would most likely adapt easily to the new

regulatory framework and thrive. As a result, bank stocks were mostly higher

Friday, prompting some skeptics to question if the legislation, in fact, would

be tough enough to rein in the industry and prevent future shocks to the economy

as a result of bad gambling.

Even architects of the bill acknowledged that it might take the next financial

crisis to truly determine the effectiveness of the changes.

On Friday morning, after a 20-hour final negotiating session, lawmakers,

Congressional aides, lobbyists and the banking industry were still sorting

through the legislative rubble of a frantic night of deal-making, edits and

adjustments that left even some of those who worked most closely on the bill

confused about exactly how some of the final details turned out. At points in

the debates, lawmakers seemed to have trouble following their own deliberations.

“Can somebody explain to me what’s in Tier 1 capital?” Representative Melvin L.

Watt, Democrat of North Carolina, pleaded, referring to the core measure of a

bank’s financial strength. “I just don’t have enough knowledge in this area.”

The White House’s desire to get a bill before the Fourth of July break drove the

day. At 11 p.m. Thursday, Representative Barney Frank, Democrat of Massachusetts

and chairman of the Financial Services Committee who presided over the

conference proceedings, began to show signs of impatience. When the senior

Republican on the committee, Representative Spencer Bachus of Alabama, asked for

another minute to finish a statement, Mr. Frank cut him off. “I would object to

that,” he snapped. “Not at 11 o’clock at night.”

As midnight turned to early morning, lawmakers cast rapid-fire votes on

amendments hastily scrawled in the margins of rejected proposals. With C-Span

carrying the proceedings live, the last half-hour of the session featured

sometimes confused lawmakers repeatedly asking about what happened to various

proposed amendments.

While the televised proceedings at times provided a remarkable window into the

minutiae of legislating, many of the deals to complete the bill were cut outside

the conference room, in private discussions between Democratic lawmakers and the

Obama administration, with some of Washington’s most influential lobbyists

trying to weigh in as best they could.

One major bank on Friday scrambled to figure out what happened to six words that

to its surprise and dismay were apparently cut from an amendment on proprietary

trading, potentially posing a threat to its business.

The final bill vastly expands the regulatory powers of the Federal Reserve and

establishes a systemic risk council of high-ranking officials, led by the

Treasury secretary, to detect potential threats to the overall financial system.

It creates a new consumer financial protection bureau, and widens the purview of

the Securities and Exchange Commission to broaden regulation of hedge funds and

credit rating agencies.

The measure restricts the ability of banks to invest and trade for their own

accounts — a provision known as the Volcker Rule, for its chief proponent, Paul

A. Volcker, the former Federal Reserve chairman — and creates a tight new

regulatory framework for derivatives, the complex financial instruments that

were at the heart of the 2008 crisis.

But in a late-hour compromise, the bill does not include the tough restrictions

on derivatives trading championed by Senator Blanche L. Lincoln, Democrat of

Arkansas, which would have forced banks to jettison their most lucrative

dealings in this area.

Instead, in a deal negotiated between Mrs. Lincoln and a bloc of House members

called the New Democrat Coalition, banks will be required to segregate their

dealings only in the riskiest categories of derivatives, including the highly

structured products like credit-default swaps based on bundles of mortgage

loans, and in certain types of derivatives that are based on commodities that

banks are already prohibited from investing in, like precious metals,

agricultural products and energy.

But derivatives that have clear business purposes like helping manufacturing

companies to hedge against the cost of raw materials or swings in foreign

exchange rates would continue to be allowed. And nonfinancial corporations would

be allowed to set up their own financial affiliates to create and trade

derivatives related to their businesses.

The derivatives deal also headed off a last-minute rebellion by some New York

lawmakers concerned about the effect of Mrs. Lincoln’s proposal on Wall Street

businesses.

“We wanted to make sure we didn’t drive all the derivative business out of New

York,” said Representative Gregory W. Meeks, a Democrat from Queens, who served

on the conference committee.

The bill also does not include some of the more draconian proposals debated in

recent months, including re-establishing a firewall between commercial and

investment banking. And the nation’s auto dealers won exemption from oversight

by the new consumer protection bureau, which will regulate most consumer

lending.

Some business groups angrily denounced the final product, saying it was

ill-conceived and would have unintended consequences harmful to the economy.

“Far from effective reform, this legislation includes provisions totally

unrelated to the financial crisis which may disrupt America’s fragile economic

recovery and increase instability and risk,” said John J. Castellani, president

of the Business Roundtable, which represents chief executives of top American

companies.

The conference report approved Friday is subject to approval by both chambers of

Congress, a process that is expected to begin on Tuesday with action by the

House and then by the Senate — where 60 votes will be required to end debate.

The vote in the conference committee was on party lines, with Democrats in favor

and Republicans opposed. House conferees voted 20 to 11 to approve the bill and

Senate conferees voted 7 to 5.

Republicans repeatedly complained that the bill would do nothing to tighten

regulation of the government-sponsored mortgage companies, Fannie Mae and

Freddie Mac, which were at the heart of much of the housing crisis.

Senator Christopher J. Dodd, Democrat of Connecticut and chairman of the banking

committee who with Mr. Frank led the negotiations, said the bill would prevent

the corporate bailouts required in 2008 and allow the United States to become a

global leader in financial regulation, potentially providing decades of

stability.

“Never again will we face the kind of bailout situation as we did in the fall of

2008 where a $700 billion check will have to be written,” Mr. Dodd said in an

interview. But he acknowledged that the effectiveness of the legislation would

be learned only over time.

“I don’t have the kind of ego that would tell you we have absolutely solved

these problems,” he said. “We won’t know until we face the next economic

crisis.”

Republicans, however, warned that the bill would extend the reach of government

too far.

At one point during debate over whether banks should be allowed to trade for

their own profit, Representative Jeb Hensarling, Republican of Texas, asked what

the issue had to do with the financial crisis. “How much riskier is proprietary

trading than investment in certain forms of residential real estate?” Mr.

Hensarling asked.

“If we’re not going to bail them out with taxpayer money, what they do with

their money is their business.”

He said, adding: “This is one more occasion where we see something in the bill

that did not have a causal role in the crisis.”

While regulatory bills often get watered down as they grind through the

legislative process and interest groups and industry press for changes, the

financial bill mostly gained strength as the debate lengthened and lawmakers

seized on public frustration that rich financial institutions, recently bailed

out by taxpayers, showed no signs of curtailing their risky practices or their

outsize pay packages.

WASHINGTON — President Obama signed a sweeping expansion of federal financial

regulation on Wednesday, signaling perhaps the Democrats’ last major legislative

victory before the midterm elections in November, which could recast the

Congressional landscape.

Within minutes of the bill signing, several Wall Street groups were leveling

criticism at the new regulations, reflecting Mr. Obama’s increasingly fractious

relations with corporate America.

The Business Roundtable complained in a statement that the law “takes our

country in the wrong direction” and may discourage investment and job growth,

echoing concerns made by the United States Chamber of Commerce and other

business organizations.

In a signal that Wall Street is ready to keep lobbying as regulators work out

the details of how to apply the new law, Larry Burton, the roundtable’s

executive director, said: “We will work with President Obama and policy makers

to ensure this legislation is implemented in a manner that continues to promote

sustainable economic growth and job creation.”

Still, Democrats and White House officials were euphoric about passage of the

legislation, a response to the 2008 financial crisis that tipped the nation into

the worst recession since the Great Depression.

The law subjects more financial companies to federal oversight and regulates

many derivatives contracts while creating a consumer protection regulator and a

panel to detect risks to the financial system.

A number of the details have been left for regulators to work out, inevitably

setting off complicated tangles down the road that could last for years.

But “because of this law, the American people will never again be asked to foot

the bill for Wall Street’s mistakes,” Mr. Obama said before signing the

legislation. “There will be no more taxpayer-funded bailouts. Period.”

He was surrounded by a group of mostly Democratic lawmakers and advocates of the

overhaul legislation, including the House speaker, Nancy Pelosi of California,

and the Senate majority leader, Harry Reid of Nevada, as well as Senator

Christopher J. Dodd of Connecticut and Representative Barney Frank of

Massachusetts, chairmen of crucial committees involved in developing the

legislation.

The White House orchestrated a major signing ceremony at the Ronald Reagan

Building across from the Commerce Department to trumpet the new law.

Mr. Obama took pains to try to show how the complex legislation, with its dense

pages on derivatives practices, will protect ordinary Americans.

“If you’ve ever applied for a credit card, a student loan or a mortgage, you

know the feeling of signing your name to pages of barely understandable fine

print,” Mr. Obama said. “But what often happens as a result is that many

Americans are caught by hidden fees and penalties, or saddled with loans they

can’t afford.”

He said the law would crack down on abusive practices in the mortgage industry,

simplifying contracts and ending hidden fees and penalties, “so folks know what

they’re signing.”

The law expands federal banking and securities regulation from its focus on

banks and public markets, subjecting a wider range of financial companies to

government oversight.

It also imposes regulation for the first time on opaque markets like the

enormous trade in credit derivatives.

It creates a council of federal regulators, led by the Treasury secretary, to

coordinate the detection of risks to the financial system, and it provides new

powers to constrain and even dismantle troubled companies.

And it creates a powerful regulator, to be appointed by the president and housed

in the Federal Reserve, to protect consumers of financial products.

The first visible result may come in about two years, the deadline for the

consumer regulator to create a simplified disclosure form for mortgage loans.

Mr. Obama acknowledged three Republican senators — Susan Collins and Olympia J.

Snowe of Maine and Scott P. Brown of Massachusetts — who broke with their party

to approve the bill, saying that they “put partisanship aside, judged the bill

on the merits and voted for reform.”

September 12, 2009

The New York Times

By ALEX BERENSON

Wall Street lives on.

One year after the collapse of Lehman Brothers, the surprise is not how much has

changed in the financial industry, but how little.

Backstopped by huge federal guarantees, the biggest banks have restructured only

around the edges. Employment in the industry has fallen just 8 percent since

last September. Only a handful of big hedge funds have closed. Pay is already

returning to precrash levels, topped by the 30,000 employees of Goldman Sachs,

who are on track to earn an average of $700,000 this year. Nor are major pay

cuts likely, according to a report last week from J.P. Morgan Securities.

Executives at most big banks have kept their jobs. Financial stocks have soared

since their winter lows.

The Obama administration has proposed regulatory changes, but even their backers

say they face a difficult road in Congress. For now, banks still sell and trade

unregulated derivatives, despite their role in last fall’s chaos. Radical

changes like pay caps or restrictions on bank size face overwhelming resistance.

Even minor changes, like requiring banks to disclose more about the derivatives

they own, are far from certain.

Coming on the same weekend as the 11th-hour bailout of the giant insurer

American International Group, and the sale of Merrill Lynch, Lehman’s failure

was the climax of a cataclysmic weekend in the financial industry. In the days

that followed, nearly everyone seemed to agree that Wall Street was due for

fundamental change. Its “heads I win, tails I’m bailed out” model could not

continue. Its eight-figure paydays would end.

In fact, though, regulators and lawmakers have spent most of the last year

trying to save the financial industry, rather than transform it. In the short

run, their efforts have succeeded. Citigroup and other wounded banks have

avoided bankruptcy, and the economy has sidestepped a depression. But the same

investors and economists who predicted, and in some cases profited from, the

collapse last fall say the rescue has come at an extraordinary cost. They warn

that if the industry’s systemic risks are not addressed, they could cause an

even bigger crisis — in years, not decades. Next time, they say, the credit of

the United States government may be at risk.

Simon Johnson, a professor at the Sloan School of Management at the

Massachusetts Institute of Technology and former chief economist of the

International Monetary Fund, said that the seeds of another collapse had already

sprouted. If major banks are allowed to keep making bets that are ultimately

backed by taxpayer guarantees, they will return to the practices that led them

to underwrite trillions of dollars in bad loans, Professor Johnson said.

“They will run up big risks, they will fail again, they will hit us for a big

check,” he predicted.

The doomsday view is far from universal.

Wall Street executives say the Lehman bankruptcy opened their eyes to the

fragility of their institutions. They note that they have pulled back on risk

and reduced leverage, creating a bigger cushion against losses. And they say

that regulators were right to support the financial industry over the last year,

rather than imposing new rules or allowing weak banks to collapse.

“There is less leverage in the entire financial system,” said David A. Viniar,

Goldman’s chief financial officer. At Goldman, $1 in capital now supports about

$14 in loans and investments, compared with $24 a year ago.

But even some senior Wall Street executives acknowledge the lack of change

surprises them, given how poorly the industry performed last fall and the degree

of government support necessary to keep it from collapsing.

“There was a general feeling that an enormous amount of additional regulation

should be put in place to prevent what happened that weekend from happening

again,” said Byron Wien, vice chairman of Blackstone Advisory Services and the

former chief investment strategist for Morgan Stanley and Pequot Capital. “So

far, we haven’t seen a lot of action.”

Robert J. Shiller, the Yale University economics professor who predicted the

dot-com crash and the housing bust, said the window for change may be closing.

“People will accept change at a time of crisis, but we haven’t managed to do

much, and maybe complacency is coming back,” Professor Shiller said. “We seem to

be losing momentum.”

Kenneth C. Griffin, founder and chief executive of the Citadel Investment Group,

a Chicago-based hedge fund that manages $13 billion, said that regulators and

lawmakers needed to impose rules so failing banks could be shut, rather than

allowed to operate indefinitely with taxpayer support.

“We’ve taken a lot of steps for the worse, and not for the better, in terms of

the structural underpinnings of our capital markets,” Mr. Griffin said. “We have

to change the rules and correct the fundamental flaws in the financial system.”

To be sure, Wall Street is not exactly as it was before the cataclysm of last

year.

Then, a dozen or so big banks formed the top tier. Now Goldman Sachs and

JPMorgan Chase are clearly the strongest, with Morgan Stanley struggling to

compete. Bank of America and Citigroup are the weakest big banks, heavily

reliant on government guarantees to survive.

“We have more separation between the healthiest and the least healthy of the big

banks,” said Darrell Duffie, a finance professor at Stanford University.

Banks have collectively raised hundreds of billions in new capital to help

cushion losses on bad loans and are taking a more prudent approach to lending

and underwriting. The worst excesses of 2006 and 2007, when banks lent hundreds

of billions of dollars against all kinds of real estate at terms that even at

the time seemed absurd, have ended.

But those changes are not unexpected. Banks typically raise lending standards

during recessions. And even if they wanted to keep up underwriting, they would

not find much of a market. Many pension and hedge funds have suffered huge

losses on mortgage-backed bonds and are hardly rushing to buy more.

Critics of the industry argue that the pullback in risk will be only temporary

without deep regulatory changes. Nassim Nicholas Taleb, a statistician, trader,

and author, has argued for years that financial firms chronically underestimate

their risks and must be managed much more cautiously. Universa Investments, a $5

billion fund in which he is a principal, made more than 100 percent profit last

year betting on the possibility of a collapse.

Mr. Taleb warns that the system has grown riskier since last fall. The extensive

government support that began after Lehman collapsed will lead investors to

assume that governments will always prevent major banks from collapsing, he

said.

So investors will lend money to the financial industry on easy terms. In turn,

financial institutions will use that cheap money to make risky loans and trades.

The banks will keep the profits when their bets pay off, while taxpayers will

swallow the losses when the bets go bad and threaten the system.

Economists call the phenomenon moral hazard. Bankers have a different term:

I.B.G. The phrase implies that by the time a deal goes sour, “I’ll be gone,”

after having received a sizable bonus.

Despite the predictions last year about pay cuts, those bonuses appear secure.

Kian Abouhossein, an analyst at J.P. Morgan in London, predicted this week that

eight major American and European banks would pay the 141,000 employees in their

investment banking units $77 billion in 2011 — about $543,000 per worker, not

far from the 2007 peak — even after minor regulatory changes are adopted.

Because the rewards are so rich, the banks will not change unless regulators and

lawmakers force them, Mr. Taleb said.

“I don’t know anyone on Wall Street who goes to work every day thinking of

anything but how to increase their bonus,” he said.

To prevent a replay of last year’s crisis, investors in financial institutions,

especially bondholders, must believe that they will lose money if banks fail,

said Sheila C. Bair, the chairwoman of the Federal Deposit Insurance

Corporation. “You need to send that very strong, clear signal to restore market

discipline,” Ms. Bair said.

But legislation that would allow regulators to close giant institutions in an

orderly fashion has been stalled for months. So too have efforts to create a

systemic regulator that would focus on the broader risk that might occur from

the ripple effects caused by the failure of one major bank.

Another proposed change would require banks to list and trade derivatives

through a central clearinghouse, just as stocks and options are traded through

exchanges, but it has yet to go anywhere.

The term derivatives encompasses a variety of financial products, including

contracts whose value changes as interest rates move and insurance that pays off

if a bond defaults. Derivatives drove the boom before 2008 by encouraging banks

to make loans without adequate reserves. They also worsened the panic last fall

because they inherently tie institutions together. Investors worried that the

collapse of one bank would lead to big losses at others.

Requiring that derivatives be traded openly sounds like a relatively small

change, but it could have important effects.

Exchange trading would open pricing for derivatives, so banks could not hide

money-losing positions. Banks would have to put up money as positions moved

against them, since the exchanges would seize and sell derivatives that were not

backed by adequate margin. That move would help avoid the situation A.I.G. faced

last year, after it wrote hundreds of billions of dollars of credit insurance

and had no money to make good on its promises when the bonds defaulted. But

critics say that even the proposed changes would not go far enough, because they

would exempt some complex derivatives from exchange trading or clearing.

Moreover, some banks oppose opening derivatives trading, because it would cut

their profits by making pricing more visible and as a consequence competitive.

For now, legislation to force derivatives trading onto exchanges has stalled,

and banks are still writing contracts with limited regulatory oversight.

“The off-exchange derivatives market is still the Wild West,” Ms. Bair said.

June 30, 2009

The New York Times

By DIANA B. HENRIQUES

A criminal saga that began in December with a string of superlatives — the

largest, longest and most widespread Ponzi scheme in history — ended the same

way on Monday as Bernard L. Madoff was sentenced to 150 years in prison, the

maximum for his crimes.

Mr. Madoff, looking thinner and more haggard than when he pleaded guilty in

March, stood impassively as Federal District Judge Denny Chin condemned his

crimes as “extraordinarily evil” and imposed a sentence that was three times as

long as the federal probation office suggested and more than 10 times as long as

defense lawyers had requested.

Though many questions still surround the case, the judge’s pronouncement offered

a brief sense of resolution, followed by a short burst of applause and one

stifled cheer from the victims who filled the soaring Lower Manhattan courtroom.

Only a few moments before, Mr. Madoff had apologized for the harm he inflicted

on the clients who had trusted him, his employees and his family. He blamed his

pride, which would not allow him to admit his failures as a money manager.

“I am responsible for a great deal of suffering and pain. I understand that,” he

said, leaning slightly forward over the polished table, his charcoal suit

sagging on his diminished frame.

“I live in a tormented state now, knowing of all the pain and suffering that I

have created.”

At the end of his personal statement, Mr. Madoff abruptly turned to face the

courtroom crowd. He was no longer the carefully tailored and coiffed financier.

His hair was ragged. His eyes were sunken into deep gray shadows. His voice was

a little raspy, and he stopped on occasion to sip water.

“I am sorry,” he said, and abruptly added: “I know that doesn’t help you.”

Nine victims, some choked by sobs or swiping at tears, told the court of the

damage he had caused, describing him as a psychopath and a monster who had

destroyed their lives.

“It feels like a nightmare that we can’t awake from,” said Carla Hirschhorn, a

physical therapist who said her daughter was juggling two jobs in her junior

year to help pay for college expenses that their lost savings were supposed to

cover.

Michael Schwartz, who said Mr. Madoff had stolen money set aside to sustain his

disabled brother, expressed the hope that “his jail cell will become his

coffin.”

In meting out the maximum sentence, Judge Chin pointed out that no friends,

family or other supporters had submitted any letters on Mr. Madoff’s behalf that

attested to the strength of his character or good deeds he had done.

Mr. Madoff returned to his cell at the Metropolitan Correctional Center in Lower

Manhattan while federal prison officials determine where he will serve his

sentence. The defense has 10 days to decide whether to appeal the sentence.

Although Judge Chin suggested that Mr. Madoff be assigned to a prison in the

Northeast, at the request of the defense, the judge said the Bureau of Prisons

would decide what kind of facility will become his permanent home.

No members of Mr. Madoff’s immediate family were in court.

In his statement, Mr. Madoff acknowledged the “legacy of shame” he has created

for his family.

His wife, Ruth, later released a statement — her first since her husband’s

arrest — expressing her grief for the victims and her sense of shock and

betrayal when she learned of the crime.

Mrs. Madoff has not been charged in the crime and insists that she did not know

of it until her husband told her just before his arrest. But she acknowledged

that her silence, imposed by lawyers protecting her own interests, “has been

interpreted as indifference or lack of sympathy for the victims.” That, she

added, “is exactly the opposite of the truth.”

She said she felt “devastated” by the harm her husband had done. “I am

embarrassed and ashamed. Like everyone else, I feel betrayed and confused,” said

Mrs. Madoff, who has forfeited all but $2.5 million in assets. “The man who

committed this horrible fraud is not the man whom I have known for all these

years.”

Many victims also accused regulators and lawmakers of betraying them for decades

by failing to stop Mr. Madoff, and failing them again by not helping them deal

with their financial hardships since they learned their savings had evaporated.

Judge Chin cautioned one speaker that those entities “are not before me,” but,

in a larger sense, the Madoff case seemed to put an entire era on trial — a

heady time of competitive deregulation and globalized finance that climaxed last

fall in a frenzy of fear, panic and loss.

The blame has been spread wide — to arcane credit-default swaps, to lax

enforcement of weak regulations, to poorly understood risks and badly managed

financial institutions.

But with his arrest on Dec. 11, Mr. Madoff, a senior statesman in the private

corridors of Wall Street who was respected for his vision and trusted by tens of

thousands of customers, put a human face on those abstractions.

Mr. Madoff’s luxurious lifestyle, including a penthouse, yachts and French

villa, all quickly became fuel for public outrage.

Every move in the case was closely watched, including his confession to his

sons, Andrew and Mark, who were in his business; his guilty plea to 11 counts of

various financial crimes in March; and his wife’s legal efforts to save some

family assets from a sweeping government forfeiture.

The fury increased in January with Congressional testimony from a whistle-blower

who had repeatedly alerted the Securities and Exchange Commission about his

suspicion that Mr. Madoff was operating a gigantic fraud. An internal

investigation is now under way at the S.E.C. to determine why the agency did not

detect Mr. Madoff’s scheme and shut it down years ago.

The S.E.C. and the Securities Investor Protection Corporation, a

government-chartered program to compensate customers of failed brokerage firms,

were criticized repeatedly in the courtroom statements by the victims on Monday,

and at a rally of victims held near the courthouse afterward.

The litigation already filed in and around the Madoff case will help shape how

regulators, the courts and SIPC respond to large-scale Ponzi scheme losses in

the future. How the losses of victims will be addressed is just one of many open

questions.

The criminal investigation is continuing, as prosecutors try to determine who

else bears responsibility for the crime. So far, only Mr. Madoff’s accountant

has been arrested on criminal charges, but securities regulators have filed

civil suits against several of his long-term investors, accusing them of

knowingly steering other investors into the fraud scheme for their own gain.

And the bankruptcy trustee has sued more than a half-dozen hedge funds and large

investors, seeking to recover more than $10 billion withdrawn from the fraud in

its final months and years. It is uncertain how much money he will be able to

recover to share among the victims and how long that effort will take.

And the sentence itself is likely to leave a mark as well, according to legal

experts on white-collar crime.

In remarks before announcing his decision, Judge Chin acknowledged that any

sentence beyond a dozen years or so would be largely symbolic for Mr. Madoff,

who is 71 and has a life expectancy of about 13 years.

But “symbolism is important for at least three reasons,” he said, citing the

need for retribution, deterrence and a measure of justice for the victims.

Judge Chin said he did not agree with the suggestion by Ira Lee Sorkin, Mr.

Madoff’s lead lawyer, that victims were seeking “mob vengeance” through a

maximum sentence.

“They are placing their trust in the system of justice,” he said, adding that he

hoped the sentence he imposed would “in some small way” help the victims to

heal.

Several former prosecutors called Judge Chin’s decision somewhat surprising but

appropriate.

“The judge sent a powerful deterrent message and an ominous signal to possible

co-conspirators,” said George Jackson III, a lawyer with Bryan Cave and a former

federal prosecutor in Chicago.

Richard L. Scheff, a lawyer with Montgomery, McCracken, Walker & Rhoads and an

assistant secretary for law enforcement for the Treasury Department, said the

magnitude of the sentence “demonstrates real concern for the harm caused by

Madoff to so many victims.”

He added, “Am I surprised? Yes, to a degree — but I strongly suspected that the

sentence would be tantamount to a life sentence.”

To Robert S. Wolf, with the law firm Gersten Savage, the sentence “sent a clear

and resounding message that Judge Chin felt that Madoff had not come clean and

told all about the enormity of his criminal activity and others who

participated.”

But James A. Cohen, an associate professor of law at Fordham, said he was

troubled by the sentence. “I don’t think symbolism has a very important part in

sentencing,” he said. “I certainly agree that a life sentence was appropriate,

but this struck me as pandering to the crowd.”

The victims who spoke in the courtroom were unanimous in their demand for a

maximum sentence, saying that Mr. Madoff had forfeited his right to live in

society. They pointed to the extent of the crime: a fraud that ensnared

millionaires, private foundations, a Nobel Prize laureate and hundreds of small

investors who lost their life savings to an investment guru they had trusted

completely.

Burt Ross, who lost $5 million in the fraud, cited Dante’s “The Divine Comedy,”

in which the poet defined fraud as “the worst of sin” and expressed the hope

that, when Mr. Madoff dies — “virtually unmourned” — he would find himself in

the lowest circle of hell.

Prosecutors said Mr. Madoff deserved the maximum term for carrying out one of

the biggest investment frauds in Wall Street history. Mr. Madoff’s lawyers said

he should receive only 12 years.

After Mr. Madoff’s victims finished speaking, his lawyer, Mr. Sorkin, said the

government’s request for a 150-year sentence bordered on absurd. He called Mr.

Madoff a “deeply flawed individual,” but a human being nonetheless. “Vengeance

is not the goal of punishment,” Mr. Sorkin said.

Even with a lesser term, Mr. Sorkin added, Mr. Madoff expects to “live out his

years in prison.”

Zachery Kouwe and Jack Healy contributed reporting.

November 20, 2008

The New York Times

By JACK HEALY

As the stock market tumbled to its lowest level in nearly six years on

Wednesday, Wall Street traders and many ordinary Americans were asking the same

question: Where, oh where is the bottom?

After a yearlong slide in stocks and a giant bank rescue from Washington, even

some pessimists had hoped that the worst might be over. But now, after the Dow

Jones industrial average fell below 8,000 on Wednesday, the financial crisis and

the bear market it spawned seem to be taking a new, painful turn.

Once again, investors’ confidence in the nation’s financial industry is draining

away. And once again, people are rushing for ultra-safe investments like

Treasuries. Many analysts agree that the short-term outlook seems grim now that

the Dow has fallen below 8,000, a level that had lured buyers again and again in

recent weeks.

“When you break through these kinds of levels, it strongly suggests there’s more

to go,” said Ed Yardeni, president of Yardeni Research.

But how much more to go? Dow 7,000? Dow 6,000? Many analysts are reluctant to

say, having been proved wrong so many times before. The Dow has lost nearly 40

percent this year, and many of its blue chips, from Alcoa to General Electric,

are down even more than that.

Much will depend on the course of the economy, but there is little good news on

that front. On Wednesday, a new report raised concern that the economy might be

beset by a debilitating decline in prices, or deflation.

But another big worry is that the credit markets, where this crisis began, are

coming under even more stress than they were before. Junk bonds, for instance,

fell to their lowest levels on record on Wednesday, driving the average yield on

these high-risk corporate bonds to more than 20 percent. Yields on Treasury

bills, meantime, fell to nearly zero. Investors were willing to accept almost no

return just to know their money was safe.

The Treasury’s benchmark 10-year bill rose 1 25/32, to 103 20/32, and the yield,

which moves in the opposite direction from the price, was at 3.32 percent, down

from 3.53 percent late Tuesday.

Another source of concern is a possible new round of forced sales by hedge

funds, seeking to raise the cash quickly to meet margin calls and redemptions of

assets by investors.

Few stocks escaped unscathed. Shares of small and midsize companies fell, as

well as those of Wal-Mart, the retailer. Energy companies plunged, as did

airlines, fast-food chains and pharmaceutical companies.

But it was financial stocks that bore the brunt of the selling, and, for many

analysts, seem the most worrisome. Financial shares are plunging far below the

levels plumbed in October, when panic gripped the markets. On Wednesday,

Citigroup, the hobbled financial giant, plunged 23.4 percent to a mere $6.40 in

an avalanche of sell orders. Once the most valuable financial company in

America, Citigroup is now worth less than U.S. Bancorp.

Big banks like Bank of America, JPMorgan Chase and Wells Fargo & — all of which,

like Citigroup, have received billions of dollars from the government — fell

more than 10 percent.

Goldman Sachs, the former employer of Henry M. Paulson Jr., the Treasury

secretary, sank to its lowest level since it went public in 1999. Analysts

predicted that Goldman, the most profitable bank in Wall Street history, would

suffer its first loss as a public company.

Even Warren E. Buffett’s Berkshire Hathaway, which owns the Geico Corporation

and recently invested in Goldman Sachs, fell 12 percent, its steepest decline in

more than two decades. The Dow Jones industrial average closed down 427.47

points or 5.07 percent, at 7,997.28. The broader Standard & Poor’s 500-stock

index closed down 6.12 percent or 52.54 points at 806.58 while the

technology-heavy Nasdaq ended down 6.53 percent at 1,386.42.

But even as markets tumbled, analysts saw few signs of capitulation, that final

burst of panicked selling that typically marks a market bottom. If anything,

Wednesday’s new lows are a sign that Wall Street has farther to fall.

“The market is still anticipating that we have not seen the worst,” said Ryan

Larson, head equity trader at Voyageur Asset Management.

After precipitous declines this autumn, Wall Street had spent the past weeks

testing its yearly lows by dipping sharply, only to rebound late in the day. The

testing and retesting prompted some optimists to hope that the markets had

finally found a foothold.

But Wednesday’s drop proved them wrong.

A gathering mass of bleak economic conditions seemed to approach the critical

point, as fears of deflation and the auto industry’s waning prospects of a

federal bailout drove financial markets into an afternoon selling frenzy.

Auto shares fell as the leaders of the three American automakers reprised their

appearance on Capitol Hill to discuss an emergency bailout and the threat of

bankruptcy. General Motors was down 10 percent, to $2.79 a share, and the Ford

Motor Company was down 25 percent, to $1.26.

Crude oil settled at a 22-month low at $53.62 a barrel, and energy stocks

followed them lower.

Wednesday’s losses followed news that consumer prices dropped 1 percent in

October, a record one-month decline, according to the Labor Department. Energy

prices, which tumbled 8.6 percent over the month, led the declines.

Meanwhile, housing starts in October fell 4.5 percent to a seasonally adjusted

791,000 from the prior month, the government reported on Wednesday. For the

year, housing starts were down 38 percent and building permits were 40 percent

lower, reflecting how the housing industry has slammed to a halt amid tumbling

home values, slumping sales and tighter credit markets.

Asian stock markets opened sharply lower on Thursday. Trade data from Japan,

Asia’s largest economy, showed big drops in exports compared with a year ago.

The Nikkei 225 index in Japan dropped 4.3 percent soon after the opening.

Similar falls were seen in South Korea, where the Kospi fell 3.9 percent.

October 30, 2008

Filed at 9:01 a.m. ET

The New York Times

By THE ASSOCIATED PRESS

HOUSTON (AP) -- Exxon Mobil Corp., the world's largest

publicly traded oil company, reported income Thursday that shattered its own

record for the biggest profit from operations by a U.S. corporation, earning

$14.83 billion in the third quarter.

Bolstered by this summer's record crude prices, the Irving, Texas-based company

said net income jumped nearly 58 percent to $2.86 a share in the July-September

period. That compares with $9.41 billion, or $1.70 a share, a year ago.

The previous record for U.S. corporate profit was set in the last quarter, when

Exxon Mobil earned $11.68 billion.

Revenue rose 35 percent to $137.7 billion.

On average, analysts expected the company to earn $2.39 per share in the latest

quarter on revenue of $131.4 billion.

Exxon Mobil's results got a boost of $1.62 billion in the most-recent quarter

from the sale of a natural gas transportation business in Germany. It also took

a special, after-tax charge of $170 million related to a punitive damages award

related to the 1989 Exxon Valdez oil spill.

Excluding those items, third-quarter earnings amounted to $13.38 billion --

nearly 15 percent above its previous profit record from the second quarter.

As expected, Exxon Mobil posted massive earnings at its exploration and

production, or upstream, arm, where net income rose 48 percent to $9.35 billion.

Higher oil and natural gas prices propelled results, even though production was

down from the third quarter a year ago.

Oil producers are coming off a quarter during which crude prices reached an

all-time high of $147.27 -- and their profits have reflected it. Crude prices,

however, have quickly fallen 50 percent from the summer's highs, and the global

economic malaise has raised questions about energy demand at least into 2009.

Some companies, especially smaller producers, are scaling back spending on new

exploration and production projects because of the uncertainty, though analysts

say that its less likely to happen at the well-heeled giants like Exxon Mobil.

Company shares rose 96 cents to $75.61 in premarket trading.

September 21, 2008

The New York Times

By DAVID M. HERSZENHORN

WASHINGTON — The Bush administration on Saturday formally proposed a vast

bailout of financial institutions in the United States, requesting unfettered

authority for the Treasury Department to buy up to $700 billion in distressed

mortgage-related assets from the private firms.

The proposal, not quite three pages long, was stunning for its stark simplicity.

It would raise the national debt ceiling to $11.3 trillion. And it would place

no restrictions on the administration other than requiring semiannual reports to

Congress, granting the Treasury secretary unprecedented power to buy and resell

mortgage debt.

“This is a big package, because it was a big problem,” President Bush said

Saturday at a White House news conference, after meeting with President Álvaro

Uribe of Colombia. “I will tell our citizens and continue to remind them that

the risk of doing nothing far outweighs the risk of the package, and that, over

time, we’re going to get a lot of the money back.”

After a week of stomach-flipping turmoil in the financial system, and with

officials still on edge about how global markets will respond, the delivery of

the administration’s plan set the stage for a four-day brawl in Congress.

Democratic leaders have pledged to approve a bill but say it must also include

tangible help for ordinary Americans in the form of an economic stimulus

package.

Staff members from Treasury and the House Financial Services and Senate banking

committees immediately began meeting on Capitol Hill and were expected to work

through the weekend. Congressional leaders are hoping to recess at the end of

the week for the fall elections, after approving the bailout and a budget

measure to keep the government running.

With Congressional Republicans warning that the bailout could be slowed by

efforts to tack on additional provisions, Democratic leaders said they would

insist on a requirement that the administration use its new role, as the owner

of large amounts of mortgage debt, to help hundreds of thousands of troubled

borrowers at risk of losing their homes to foreclosure.

“It’s clear that the administration has requested that Congress authorize, in

very short order, sweeping and unprecedented powers for the Treasury secretary,”

the House speaker, Nancy Pelosi of California, said in a statement. “Democrats

will work with the administration to ensure that our response to events in the

financial markets is swift, but we must insulate Main Street from Wall Street

and keep people in their homes.”

Ms. Pelosi said Democrats would also insist on “enacting an economic recovery

package that creates jobs and returns growth to our economy.”

Even as talks got under way, there were signs of how very much in flux the plan

remained. The administration suggested that it might adjust its proposal,

initially restricted to purchasing assets from financial institutions based in

the United States, to enable foreign firms with United States affiliates to make

use of it as well.

The ambitious effort to transfer the bad debts of Wall Street, at least

temporarily, into the obligations of American taxpayers was first put forward by

the administration late last week after a series of bold interventions on behalf

of ailing private firms seemed unlikely to prevent a crash of world financial

markets.

A $700 billion expenditure on distressed mortgage-related assets would roughly

be what the country has spent so far in direct costs on the Iraq war and more

than the Pentagon’s total yearly budget appropriation. Divided across the

population, it would amount to more than $2,000 for every man, woman and child

in the United States.

Whatever is spent will add to a budget deficit already projected at more than

$500 billion next year. And it comes on top of the $85 billion government rescue

of the insurance giant American International Group and a plan to spend up to

$200 billion to shore up the mortgage finance giants Fannie Mae and Freddie Mac.

At his news conference, Mr. Bush also sought to portray the plan as helping

every American. “The government,” he said, “needed to send a clear signal that

we understood the instability could ripple throughout and affect the working

people and the average family, and we weren’t going to let that happen.”

A program to help troubled borrowers refinance mortgages — along with an $800

billion increase in the national debt limit — was approved in July. But

financing for it depended largely on fees paid by Fannie Mae and Freddie Mac,

which have been placed into a government conservatorship.

Representative Barney Frank, Democrat of Massachusetts and chairman of the House

Financial Services Committee, said in an interview that his staff had already

begun working with the Senate banking committee to draft additions to the

administration’s proposal.

Mr. Frank said Democrats were particularly intent on limiting the huge pay

packages for corporate executives whose firms seek aid under the new plan,

raising the prospect of a contentious battle with the White House.

“There are going to be federal tax dollars buying up some of the bad paper,” Mr.

Frank said. “They should accept some compensation guidelines, particularly to

get rid of the perverse incentives where it’s ‘heads I win, tails I break even.’

”

Mr. Frank said Democrats were also thinking about tightening the language on the

debt limit to make clear that the additional borrowing authority could be used

only for the bailout plan. And he said they might seek to revive a proposal that